Pony.ai’s Robotaxis and the Long Road Ahead

Robotaxi observers worldwide believe one thing about the industry in China: It’s moving aggressively. NYT dubbed Wuhan “the world’s largest experiment in driverless cars,” thanks to significant government support both in terms of regulations for testing and data collection.

The hottest Chinese startups are going public in the US, too. Most notably, Pony.ai 小马智行 made its Nasdaq debut the day before Thanksgiving. The company recently said it would expand its robotaxi fleet from 250 to 1,000 in 2025, significantly growing its commercialization prospects.

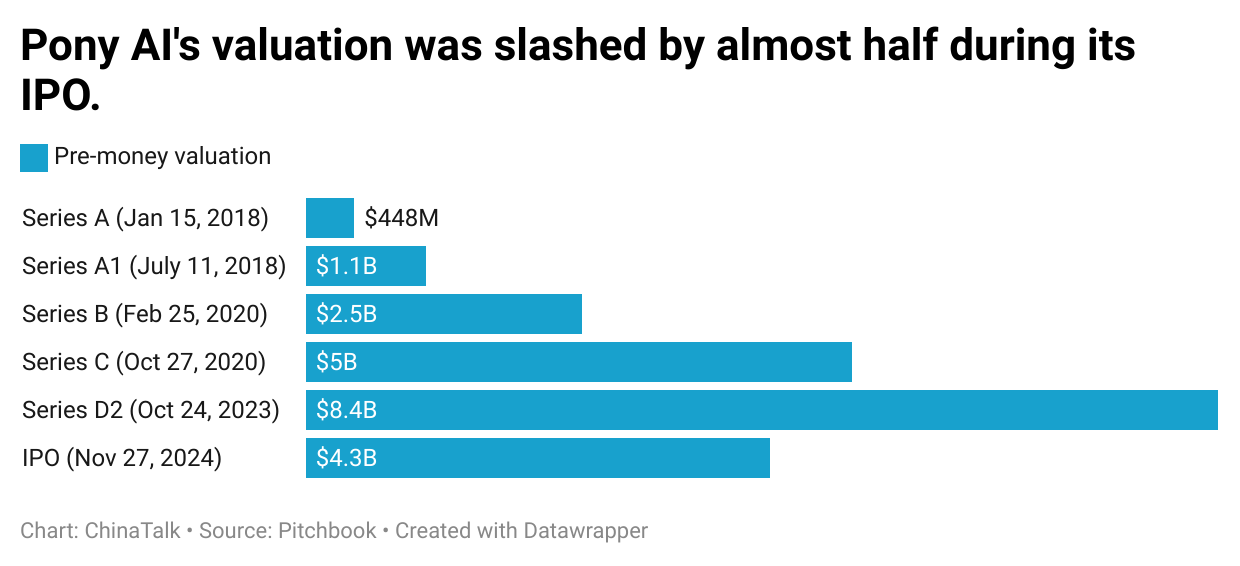

Pony.ai’s IPO was valued at $5.25 billion. Not peanuts, but less than its $8.5 billion Series D. Compared to its heyday, Pony is being tested by a harsh market reality and may face stringent international regulatory barriers as it tries to bring its technology abroad. To understand the future of Chinese AVs, ChinaTalk dove deep into the industry’s history and interviewed both cofounders of Pony.ai. We get into:

Pony.ai’s rise to China’s leading robotaxi company

How broader changes in the robotaxi industry and Chinese companies’ fundraising environment affect Pony.ai’s IPO

The challenges of commercialization for Pony.ai

Pony.ai’s plans for overseas expansion amidst international hesitance to accept Chinese AV

Past: The Top Horse in the Chinese AV Race

In late 2016, James Peng 彭军 and Tiancheng Lou 楼天城 left their jobs at Baidu’s autonomous driving department to found Pony.ai, a company that develops Level 4 autonomous driving technology. L4 refers to the stage of automation where a vehicle can drive without a human driver.

The self-driving industry boomed during those years. Hundreds of startups were founded across a complex web of transportation systems, and autonomous driving was largely believed to be the first momentous application of artificial intelligence in the pre-GPT era. Uber started its self-driving unit in 2015 and acquired Otto, a self-driving truck startup, in 2016. The same year, Google’s self-driving unit, where Lou used to work, became Waymo and publicly demonstrated its technology. Almost every major automaker announced partnerships to develop these technologies or invested in a startup.

In China, Baidu started investing in autonomous vehicle research in 2013 and began the Apollo project to develop its own driverless vehicles in 2017. Many of the big names in China’s robotaxi industry came from Baidu, including the founders of Pony.ai and WeRide.

Thanks to the strong technical backgrounds of Pony’s founders, China’s biggest investors were immediately interested. HongShan 红杉中国 (formerly Sequoia China) led Pony’s seed round in 2017. Then in 2020, Toyota participated in Pony’s Series B, and later became a key partner in Pony’s attempts to commercialize its robotaxi tech: Pony develops self-driving software and hardware, and Toyota provides the vehicles.1

Pony also expanded quickly in its first five years. In 2018, Pony became the first company in China to launch a public-facing robotaxi service (ie, fully autonomous vehicles with safety drivers) regularly operating in Guangzhou, while obtaining a permit to test in Beijing. Around the same time, the company started to explore robotrucks and established a trucking division in 2020. In 2021, Pony began to remove safety drivers in some of its robotaxis in Guangzhou.

At the end of 2020, Pony was valued at $5.3 billion and raised $2.5 billion in Series-C funding thanks to investments from sovereign wealth funds such as Ontario Teacher’s Pension Plan and Brunei Investment Agency. By June 2021, the company was on the verge of initiating an IPO, but launch plans came to a grinding halt when SEC asked for a “pause” on US IPOs of Chinese companies.

That marked the beginning of a downturn for many USD venture funds in China and left Pony in an awkward situation: Autonomous vehicles are capital-intensive and R&D-driven, and the commercialization process had only just started. Given the company’s high valuation, there were doubts about whether Pony could drum up more interest from private funds without an IPO.

But Pony wasn’t horsing around — it closed a $1.1 billion Series D at a valuation of $8.5 billion. In October 2023, amid a bonanza of Middle Eastern investments in Chinese EV and AV companies, Pony secured another $100 million from the financial wing of NEOM, Saudi Arabia’s urban desert megaproject.

Present: Pitched Promises Meet Commercialization Challenges

In its IPO filing, Pony disclosed the current scale of its operations. And these numbers are modest, to say the least.

Pony has a fleet of around 250 robotaxis operating across four tier-one cities in China: Beijing, Guangzhou, Shenzhen, and Shanghai. It’s charging fares for fully driverless rides in the first three. During the first half of 2024, each fully driverless robotaxi received an average of 15 orders per day.

By comparison, Waymo currently operates a fleet of over 700 vehicles which complete more than 150,000 rides every week in metro Phoenix, San Francisco, and Los Angeles. Baidu has a fleet of 500 vehicles in Wuhan alone.

In an interview, Tiancheng Lou told me that only three companies have achieved L4 self-driving: Waymo, Baidu, and Pony.

AV companies are facing a tough reality in 2024. General Motors just axed funding for Cruise, the AV startup it acquired a decade ago. Cruise had been burning through money, and after a major accident involving a fully autonomous vehicle, it was only testing robotaxis very slowly, one city at a time, without offering public-facing services. Other automakers have been similarly unable to pony up the necessary cash for AV development.

For Pony.ai, there is an additional level of complexity, because unlike Apollo, Waymo, and even Amazon-owned Zoox, Pony is not backed by a major tech giant. It needs funding more urgently, perhaps, than any other AV company.

“It is my disadvantage,” Lou told me. “I have to wait until the cost structure is stable to add a car. But that also means that I have to do well.”

By “cost structure,” Lou was referring to per-vehicle operating margin. Usually, that’s the difference between passenger fare and per-vehicle cost which includes maintenance, research, and manufacturing. Lou and Peng were optimistic that the margin would turn positive in 2025. In other words, when adding a new vehicle to the robotaxi fleet, the company does not lose money.

But right now, Pony.ai is still a money-losing business: While revenue rose from $68 million in 2022 to $71 million in 2023, net loss attributable to the company was $148 million and $124 million in these two years respectively. R&D still accounts for the highest percentage of Pony’s operating expenses, adding up to over $123 million in 2023.

The good news is that losses have begun to narrow over time. But Pony’s IPO filing promise — that robotaxis would be the company’s main source of revenue — is still far from becoming a reality.

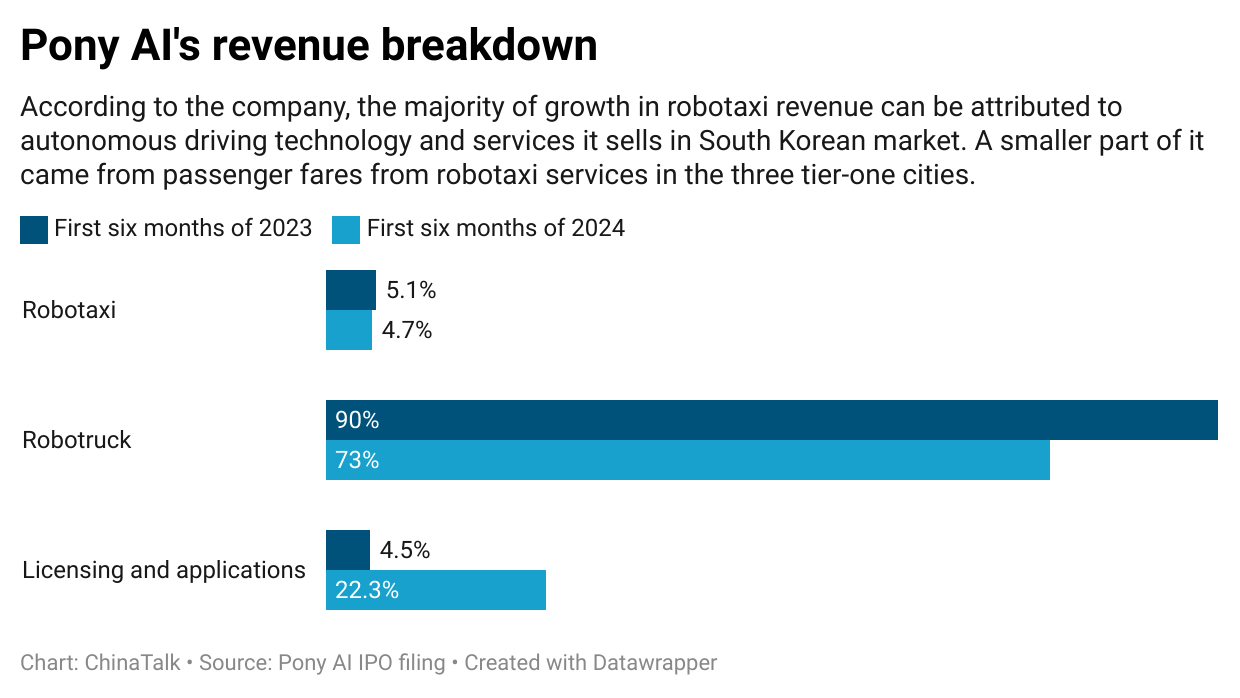

Pony has about 190 robotrucks, which generated 73% of its revenue over the first six months of 2024. Much of this new revenue came from transportation fees collected by Cyantrain, a joint venture founded by Pony and Sinotrans, for freight orders fulfilled by robotrucks.

Lou told me that it’s harder to scale robotrucks than robotaxis. The hardest part about robotaxi is the technology, he said. As long as the technology is mature enough to allow the vehicles to drive fully autonomously, it’s not hard to build tens of thousands of vehicles with that capacity. However, when it comes to trucks, which are larger and faster, there is a higher safety standard to meet.

Another way to diversify revenue is by selling so-called L2++ technology, which Pony started doing in 2022. L2++ refers to technology that assists human drivers instead of replacing them, which is sold to OEMs.

Other Chinese self-driving startups are choosing this road as well. WeRide went public in October but only sold 3 robotaxis and 19 robobuses in 2023. Revenue from these products declined by almost half between 2021 and 2023, from 101 million yuan to 54 million yuan. And even these numbers are padded by government contracts (“local transportation service providers”) as opposed to public-facing, fared robotaxi services. Meanwhile, WeRide’s service revenue (eg, L2 to L4 technical support and R&D services) increased from 36 million yuan to 347 million yuan during the same period.

Regardless, Pony clearly benefits from a Nasdaq IPO: US investors are likely more lenient about the intensive time and capital requirements of self-driving vehicle development. Several investors told me that they didn’t expect a newly minted tech IPO to be profitable.

But investors won’t wait forever — eventually, AV shareholders will push for a path to profitability as proof that they bet on the right horse.

Future: Overseas Expansion vs International Regulation

Pony is already the leading robotaxi company in China, with operations in four tier-one cities, but questions remain about the company’s post-IPO international expansion plan. Pony now has research centers in Silicon Valley and Luxembourg, and potential operations in Hong Kong, Singapore, South Korea, Saudi Arabia, UAE, and Luxembourg.

“We have set up a layout of operations in these places,” James Peng said in an interview. “The ‘layout’ doesn’t necessarily mean that the cars are already there. It’s more about technological partnerships or selling parts. In some of these places, the cars are still on the way, but eventually, we will have them.”

The market is still very new, so Pony is still adjusting their overseas investment, Peng added.

Pony is also partnering with Uber to offer driverless car services in overseas markets, although Uber has also inked cooperation agreements with Waymo, Cruise, and Wayve. Before Pony’s IPO, Bloomberg reported that Uber was in talks to invest in the startup’s offering.

Pony doesn’t have any immediate plan to expand operations to the US. California suspended Pony’s California driverless testing permit in the fall of 2021 after a reported collision in Fremont, a one-party incident where the vehicle hit a street sign. (The state’s Department of Motor Vehicles also temporarily revoked Pony’s permit to test vehicles with a driver in 2022, alleging the company’s failures to monitor the driving records of safety drivers, before the permit was reinstated at the end of 2022.)

“We are mostly focusing on China, because there is a large enough market, sufficient demand, and policymakers are supportive,” Peng told me.

It is not easy to compare self-driving regulations between the US and China. I’ve heard US transportation officials saying that the Chinese government is more proactive in regulating self-driving tech. To me, the main difference is that the Chinese government has adopted a more top-down approach to regulating autonomous vehicles. The first set of major guidelines for testing robotaxis on public roads was released in 2018.

Then in November 2023, China’s Ministry of Industry and Information Technology and three other departments jointly issued the “Notice on Carrying Out Pilot Work for the Access and Road Usage of Intelligent Connected Vehicles.” This notice focuses on conducting access pilot programs and road usage pilot programs for intelligent connected vehicles with L3 (where the driver should still remain in the vehicle) and L4 autonomous driving systems within designated areas.

More than 30 Chinese cities and provinces have released their own sets of guidelines and permitting schemes for the testing and operation of robotaxis. Some are more supportive than others. Yet, in all cities, robotaxis still can only operate on designated public roads, which could negatively impact attempts to scale.

Wuhan, sometimes called the “robotaxi city of China,” is arguably also the largest testing ground for robotaxis in the world, as the opening testing area for the technology has reached about 3,000 square kilometers (over 1,160 square miles.) Even then, Baidu has yet to reach its goal of deploying 1,000 robotaxis in the city within 2024. (The consensus thus far is that at least 1,000 fully autonomous robotaxis are needed in a city to achieve scalable commercialization.) An expert from Baidu told Huxiu that the peak of robotaxi commercialization will arrive between 2028-2030.

In both US and China, “The policies are more advanced than technological development,” said Lou.

ChinaTalk is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In its IPO filing, Pony said it established a joint venture with Toyota, where the latter would supply vehicles as a fleet company. This is similar to Waymo’s partnership with Jaguar. Toyota is the biggest shareholder of Pony.ai.

")