In 2017, Hangzhou-based robotics firm Unitree 宇树科技 launched its first quadruped, Laikago. Laika was the name of the Soviet space dog onboard Sputnik 2, and the American English pronunciation of “go” is similar to that of the Chinese word for dogs, 狗 gǒu. Unitree’s battery-powered tribute to Laika wasn’t fuzzy, but walked on four feet and navigated through basic obstacles.

Unitree founder Wang Xingxing 王兴兴 has long held faith in the potential of robotic canines. Since 2020, when Unitree started gaining media attention, he has insisted in multipleinterviews that humans are drawn to four-legged creatures and will have a natural fondness for their artificial counterparts.

Wang Xingxing with a Laikago in 2017. (Source: Bilibili)

Fast forward to 2026, and Unitree has just filed for a $610-million IPO on the Shanghai Stock Exchange. The company is a household name in China after its humanoid robots performed dances at the CCTV Spring Festival Gala for two consecutive years and counting. Through their IPO disclosures (investor prospectus and response letter to the Shanghai Stock Exchange’s inquiries), we get some answers to important questions about the development of embodied AI.

How is Unitree profitable?

Where is diffusion happening inside China, aside from dancing on TV?

Are Chinese robotics companies content to lead in hardware and applications, or do they also see themselves as pursuing some kind of generalized “frontier”?

And finally, what does this all mean for US-China dynamics in robotics?

What’s the money maker?

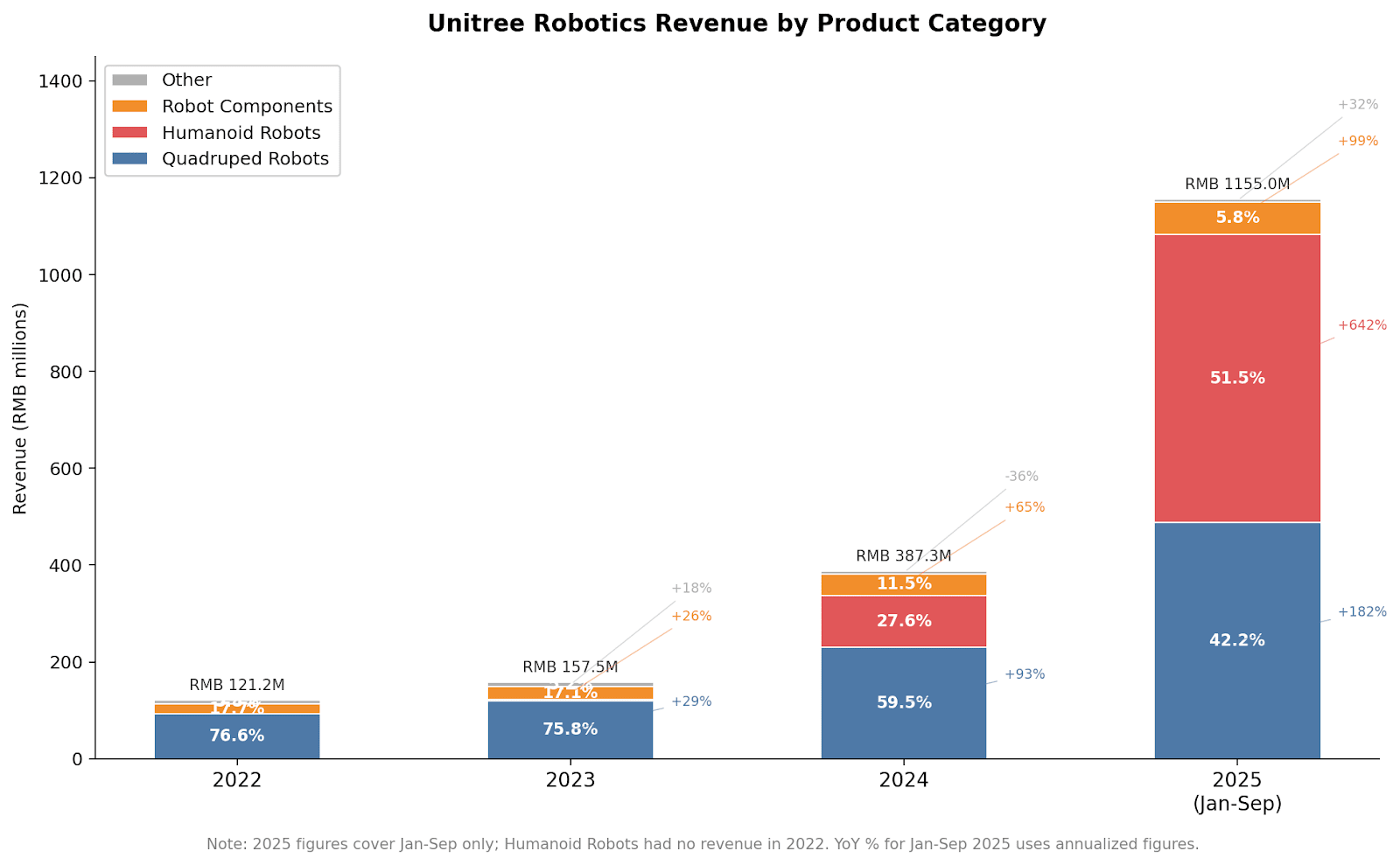

One of the most notable things about Unitree is the fact that it actually makes money. Unprofitability is a near-universal challenge because AI robotics, despite massive advances in the past few years, is still an early-stage technology. Mass adoption has not yet arrived; pathways out of bottlenecks like data are uncertain; and important safety standards have not caught up. Even shipping products consistently can be a challenge for some companies in the space, let alone manufacturing at scale and booking reliable customers.

This context is why observers have found Unitree’s ability to turn a profit remarkable. Not only has the company’s net profit been positive since 2024, but from 2024 to 2025, its net profit grew by 204.29%. A look at its growth, broken down by product category, reveals the most significant source of this revenue explosion: humanoids.

It’s perhaps ironic that, despite the company’s longstanding work in quadrupeds, it is humanoids that have catapulted its business model to success. By meeting genuine demand in academia — and staging an especially strong marketing campaign in front of the Chinese public — Unitree has transformed itself into a humanoid frontrunner. Some analyses trace their potent commercialization drive back to Unitree’s origins. Wang Xingxing’s cofounder Chen Li 陈立, who was Wang’s classmate throughout both their undergraduate and Master’s programs, worked in international sales for the Hangzhou-based, partly state-owned surveillance tech giant Hikvision (海康威视) before joining Unitree. Hikvision has been extremely successful at expanding internationally (including in the US before it was added to the Entity List over its involvement in human rights abuses against ethnic and religious minorities in China). Investors have told Chinese media that Chen’s experience is an important asset for Unitree’s global commercialization, driving sales to governments and businesses in particular.

Unitree has earned name recognition in the West, but it is far from the only Chinese robotics company meaningfully shaping the future of embodied AI. In fact, it is part of an increasingly competitive market for AI-powered robots. Among listed peers, UBTECH and Dobot are major competitors named in Unitree’s prospectus. A fellow member of the “Hangzhou Six Dragons,” DEEP Robotics, is betting big on scenario-adapted applications, while AgiBot, by some estimates, shipped even more humanoid units last year than Unitree did.

In their response to the Shanghai Stock Exchange’s inquiry letter, Unitree emphasized in-house development of hardware parts as its key strategy for cutting costs. Unitree designs, builds, and assembles most components (other than commodity components like battery cells, flash storage, and the core computing board) in-house. It does offer outsourced alternatives for add-ons like LiDAR, cameras, and dextrous hands, but has also developed in-house options for all of these.

Where are the robots?

Unitree’s most reliable customers are universities, research institutions, and other companies conducting research into robotics. Its hold on academic customers worldwide is so firm that it’s caused alarm among DC policymakers. In May 2025, the China Select Committee called for Unitree to be designated as a “Chinese military company” and to be added to the Entity List.

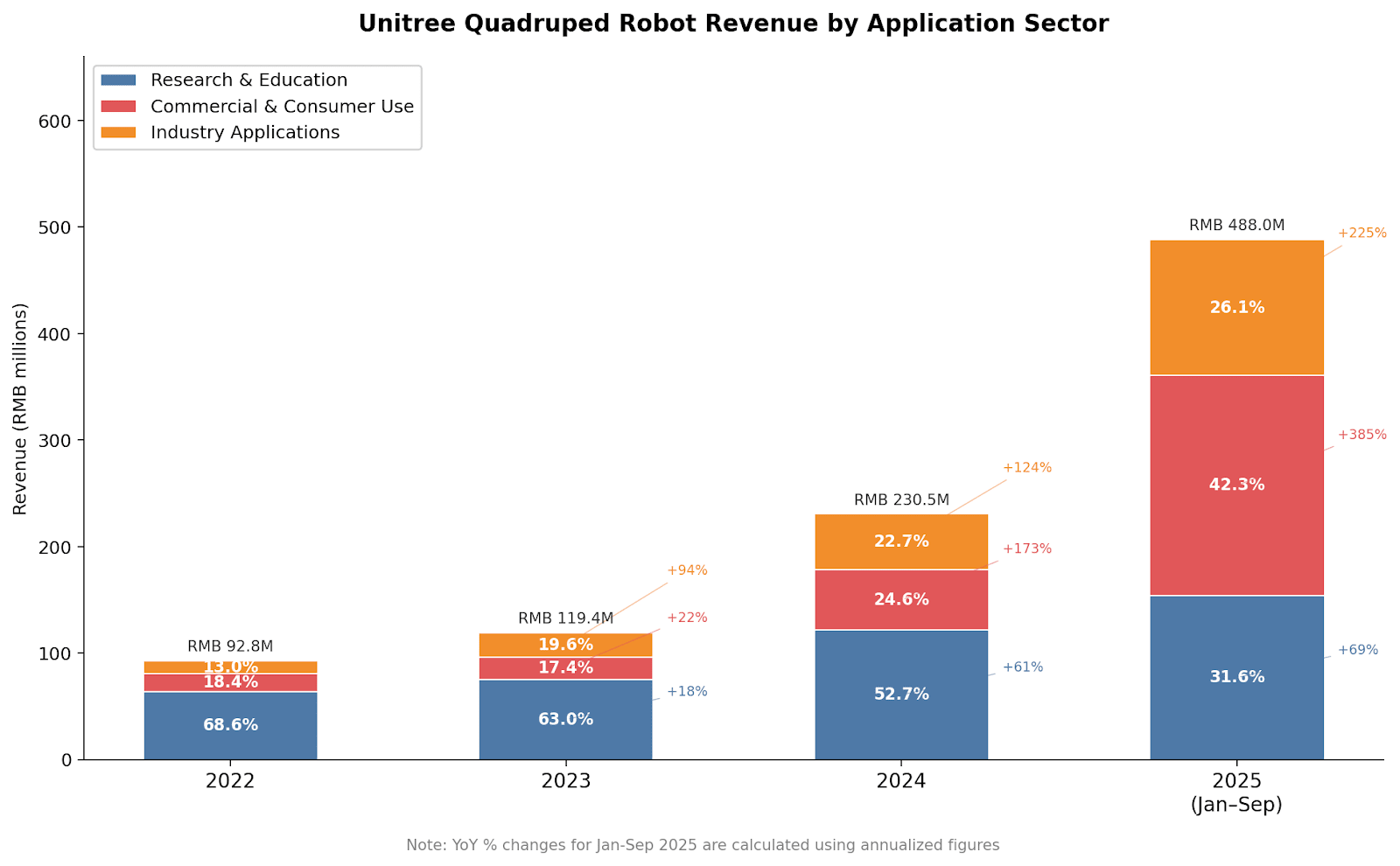

The data Unitree disclosed about its revenue sources, however, paints a more complex picture. For quadrupeds, the research and education sector has been the company’s most reliable source of revenue since at least 2022 (IPOs generally do not require companies to disclose audited financial statements from more than three years ago). But starting in 2024, revenue from both commercial and industry customers more than doubled. Consumer sales revenue nearly quadrupled year-on-year in only the first nine months of 2025.

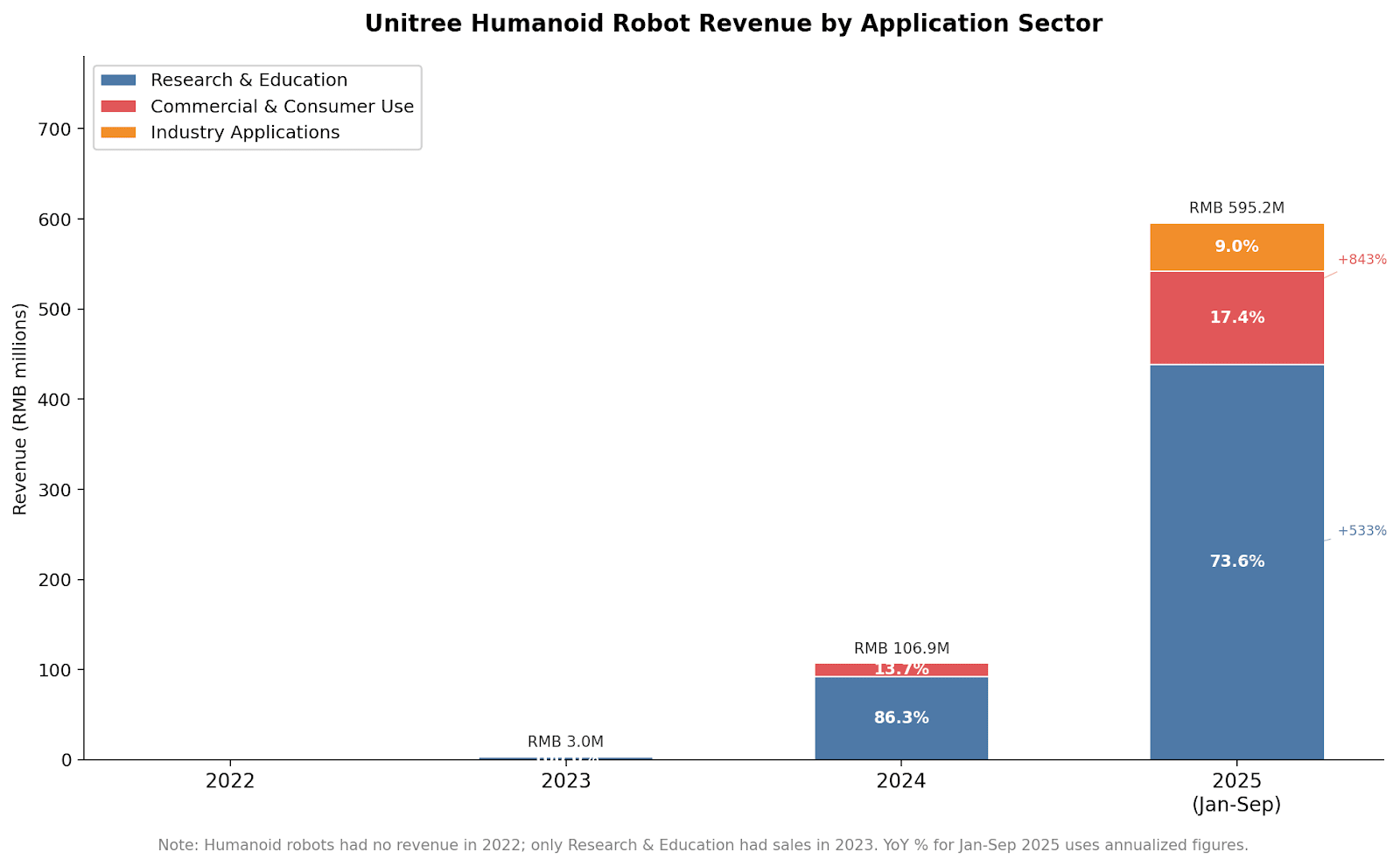

A similar, if more compact, story emerges for humanoids as well. Demand still largely comes from researchers and educational institutions, but commercial and industrial demand has grown from a near-zero starting point on a seemingly exponential trajectory since 2024. Consumers are especially excited about humanoids due to Unitree’s successful marketing of the concept. Industrial applications of humanoids are more limited compared to those of quadrupeds, but are also appearing.

What, exactly, are people doing with these robots? “Research & Education” encompasses sales to researchers, who use Unitree hardware and platforms to conduct their own experiments. The “Commercial & Consumer Use” and “Industry Applications” categories roughly map onto B2C and B2B sales, respectively. According to Unitree, non-academic consumers who buy their robots mostly do so “for show”: they’re deploying these robots as attractive promoters in retail settings, at tourist sites, and in performances and exhibitions. Some use them as novelty companions.

Applications in industry are more interesting. Quadrupeds are deployed as “smart inspectors” in power grids, subway tunnels, and gas pipelines. They can also assist in harsh settings like emergency response and outdoor surveys, and complete manufacturing and logistical tasks. E-commerce firm JD.com is Unitree’s biggest corporate customer. Humanoids, according to Unitree, are being used for inspections and manufacturing as well, though in a more limited capacity because the technology is less mature. Unitree expects consumer demand for humanoids to grow in the medium term, but we will have to wait a while longer for genuinely useful humanoids on the factory floor.

Is Unitree… AGI-Pilled?

Received wisdom in robotics has it that the US leads in software-related research, while China’s strength is in hardware. The implication is that the US is likely to reach “generalized” machine intelligence in the physical world faster than China, but — in the meantime — Chinese companies could get to practical applications faster through quick iterations inside an unparalleled manufacturing ecosystem.

Unitree’s business model is often quoted as direct evidence of this dynamic, and it is indeed true that hardware is the crux of Unitree’s success. But does that mean Unitree, and the Chinese robotics industry writ large, has less interest in generalizability or the intelligence frontier? The IPO disclosures indicate otherwise.

Unitree called on incoming investors to “realize humanity’s ultimate dream — AGI” 实现人类最终极的梦想—AGI with them. Their lawyer-drafted definition of AGI is “a form of intelligence that possesses general cognitive capabilities comparable to those of humans, capable of understanding, learning, and executing intellectual tasks across any domain, and autonomously reasoning, planning, making decisions, and continuously learning in unknown environments.”

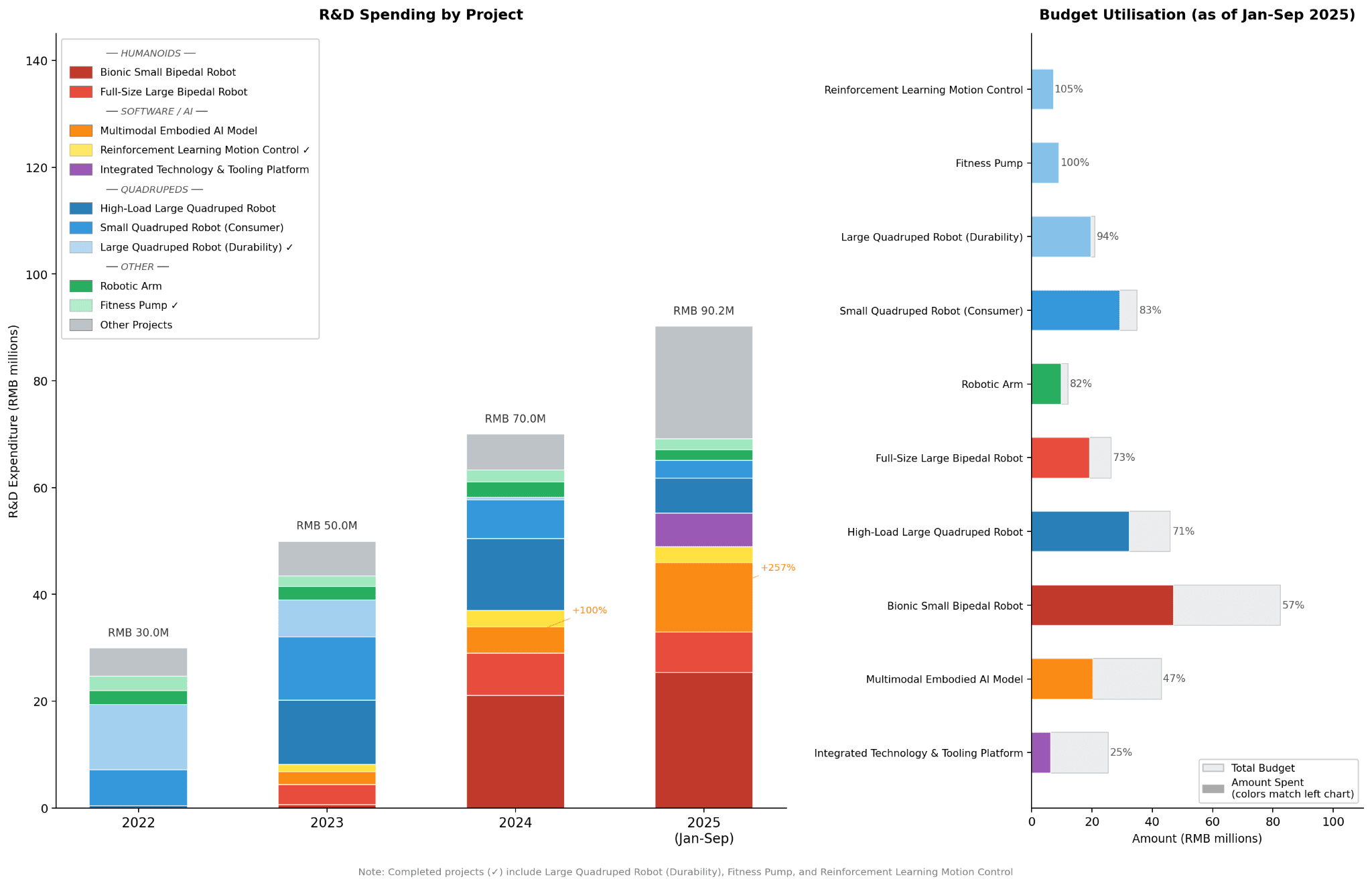

The financial reality tells us that most of Unitree’s R&D budget has gone to hardware. This is clearly downstream of their aforementioned focus on developing as many components in-house as possible to cut costs.

However, it’s important to notice in the chart above that Unitree’s R&D expenditure on “Multimodal Embodied AI Model” — the “big brain” of its robots — increased exponentially between 2024 and 2025, while other areas of R&D have grown at a steadier pace. Unitree is clearly ambitious about developing its models, even if it is known mostly for its hardware business.

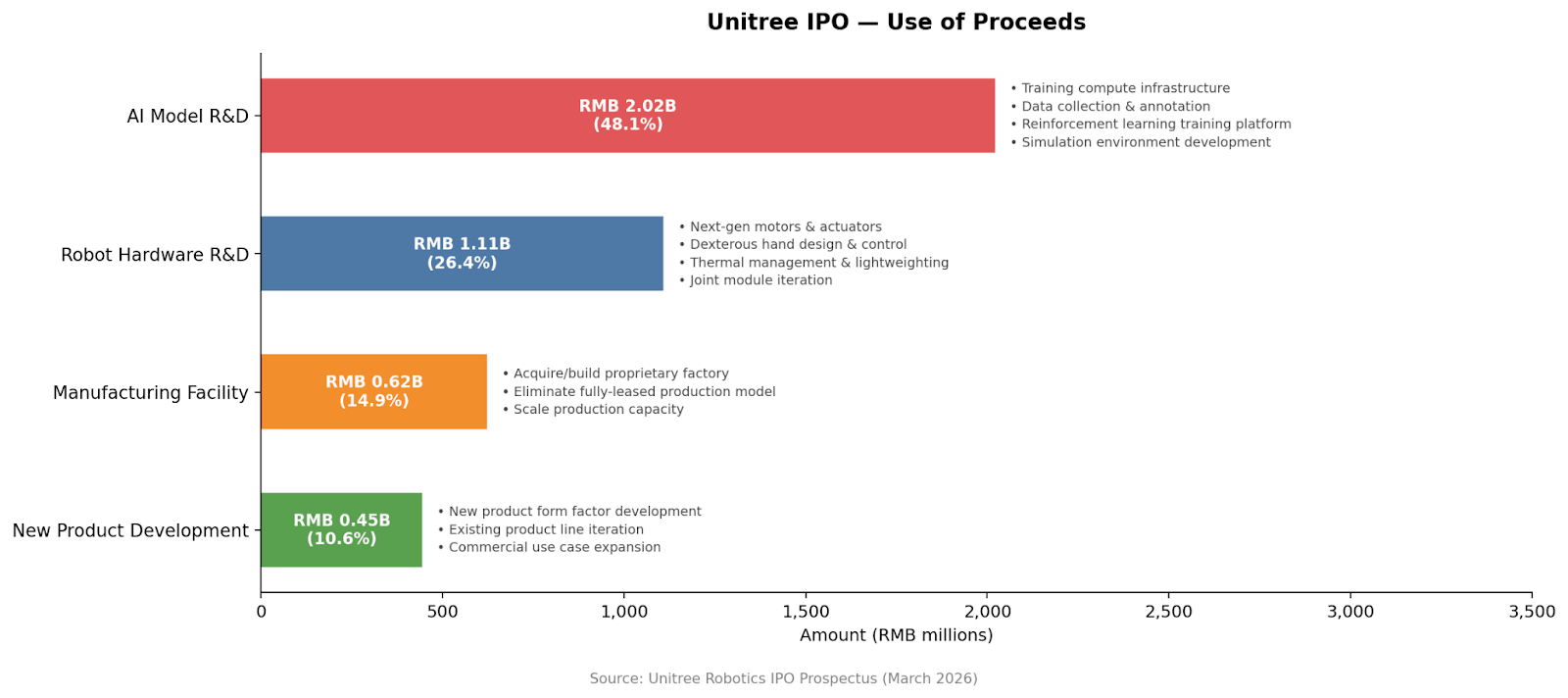

This becomes clearer when we look at Unitree’s plan for using the 4.2 billion RMB (around 607.7 million USD) raised through the IPO. Unitree’s stakeholders approved the following distribution in early 2026:

Nearly half of the IPO’s proceeds will be spent on training AI models over the next three years. That’s around 673 million RMB per year, which is not quite comparable to more well-known model makers (MiniMax, for example, spent around 1.75 billion RMB on R&D last year) but still a significant amount that signals long-term software ambitions.

Unitree currently owns no real estate, but plans to build its own factory with IPO proceeds. Per its disclosures, it has already secured a nod of approval from Hangzhou’s Binjiang District 滨江区 and plans to build there. Transitioning from an all-leased manufacturing model to proprietary manufacturing facilities is in line with their emphasis on in-house development and increasing production efficiency.

What comes next?

These disclosures answer many factual questions about Unitree’s business model, but raise more fundamental questions about the future of automation, US-China competitive dynamics, and both countries’ big bet on AI.

Question one: What will come of Unitree’s “AGI” ambitions? A public company is required to either use proceeds as stated in official disclosures, or publicly justify any changes. (Shareholders can vote to reappropriate funds, but unauthorized deviations could invoke China’s securities law and trigger scrutiny from the Stock Exchange.) Barring major issues, we should expect Unitree to spend handsomely on model training and development for the next three years. The biggest challenge will be making sure that these investments produce consequential returns. This uncertainty is not exclusive to Unitree; no one knows what the next three years will bring. But Unitree has now put itself on a path away from hardware-first and towards a more diversified strategy. This is, of course, risky, but relying on academia’s demand for hardware is no longer secure.

Question two: Will America turn against Unitree? A “Chinese military company” designation, which places companies into the annually-updated 1260H list, would merely exclude Unitree from contracting with the Department of Defense, but being placed on the Entity List would subject it to US export controls. Neither designation would prevent Unitree from selling to American customers outright, but they would hobble the company’s growth. As Unitree’s own prospectus describes:

Throughout the reporting period, revenue from overseas markets consistently exceeded 35% of total revenue. Should the United States continue to intensify trade and tariff policies that materially disadvantage Chinese exporters, or place the company on restricted lists governing procurement partnerships or technology export controls, the company faces the risk of being unable to sustain high growth in overseas sales — and potentially suffering an overall decline in performance. … Given uncertainty in industrial trade policy and the international political environment, any adverse shifts in external supply chain conditions or overseas market controls — compounded by further escalation of US trade restrictions and export control measures — could negatively affect the company’s ability to procure imported materials and maintain technology partnerships.

Policymakers eager to run “Trojan horse tech” out of America have to reckon with the dilemma that, for academic researchers at the forefront of embodied AI, there are few alternatives to Chinese-made hardware and platforms; Unitree is simply the most successful of the lot. Affordability and reliability are the most important factors for nonprofit academic labs. Robotics research is also a rough-and-tumble affair: there is wear and tear, and I’ve had researchers and students show me bruises they’ve sustained on the job from handling heavy humanoids. Unitree’s scale, consistency, and pricing meets academics where they are. Moreover, Unitree has been cultivating its relationships with international researchers long before the reporting periods of these IPO disclosures. The company started shipping internationally in 2018, and some of the earliest buyers of its quadrupeds were university research labs.

Imagine writing code for a dishwasher without dishwashers to test the code on. That’s a massively oversimplified comparison, but it is the same proposition in spirit. If Washington severs this symbiotic relationship, it will almost certainly make it harder for American researchers to maintain their lead in the software side of embodied AI.

Finally, question three: Can Unitree keep its lead inside China? As mentioned earlier, the company has formidable challengers in its own backyard, and has had to continuously trim costs to stay competitive. DEEP Robotics also joined the leagues of profitable companies in 2025. AgiBot’s CEO said at the end of last year that the company’s total sales revenue in 2025 likely exceeded 1 billion RMB. Up until now, Unitree’s success is arguably a case of first-mover advantage. Many more companies are taking up the Unitree playbook, and the future of robotics in China is far from determined.

If you aren’t yet ready to open your home to a robot dog, the company also sells fitness equipment inspired by robotics technology…

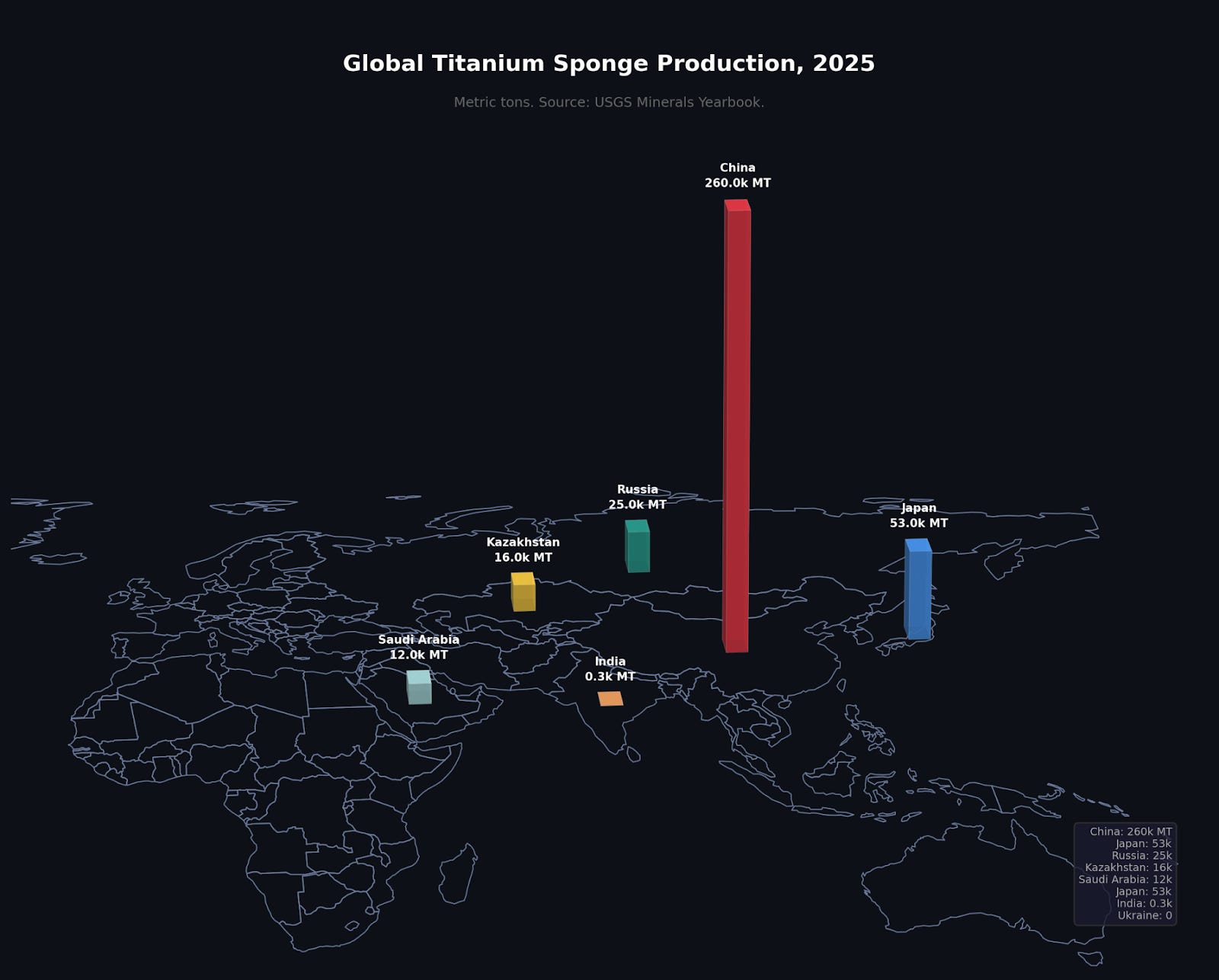

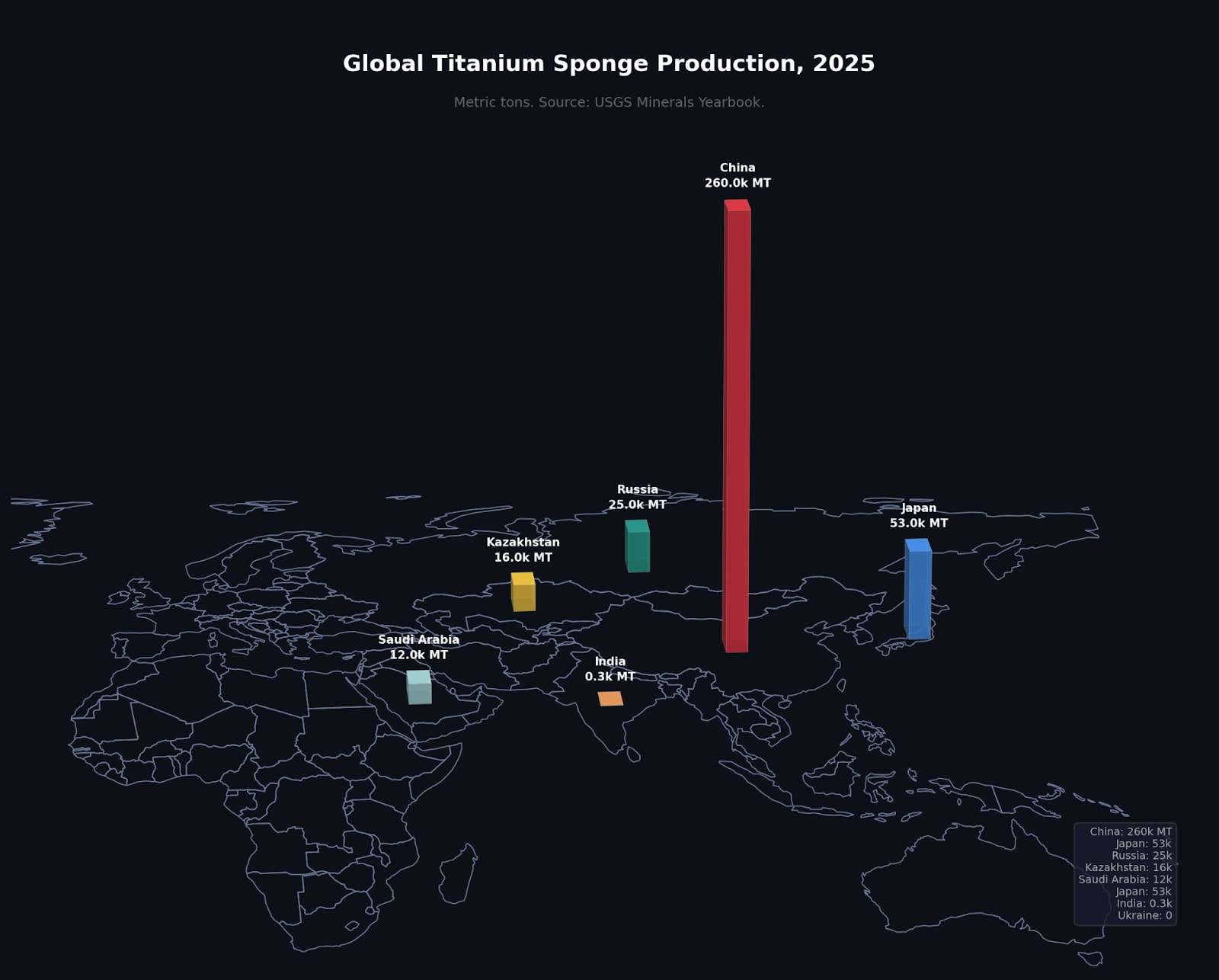

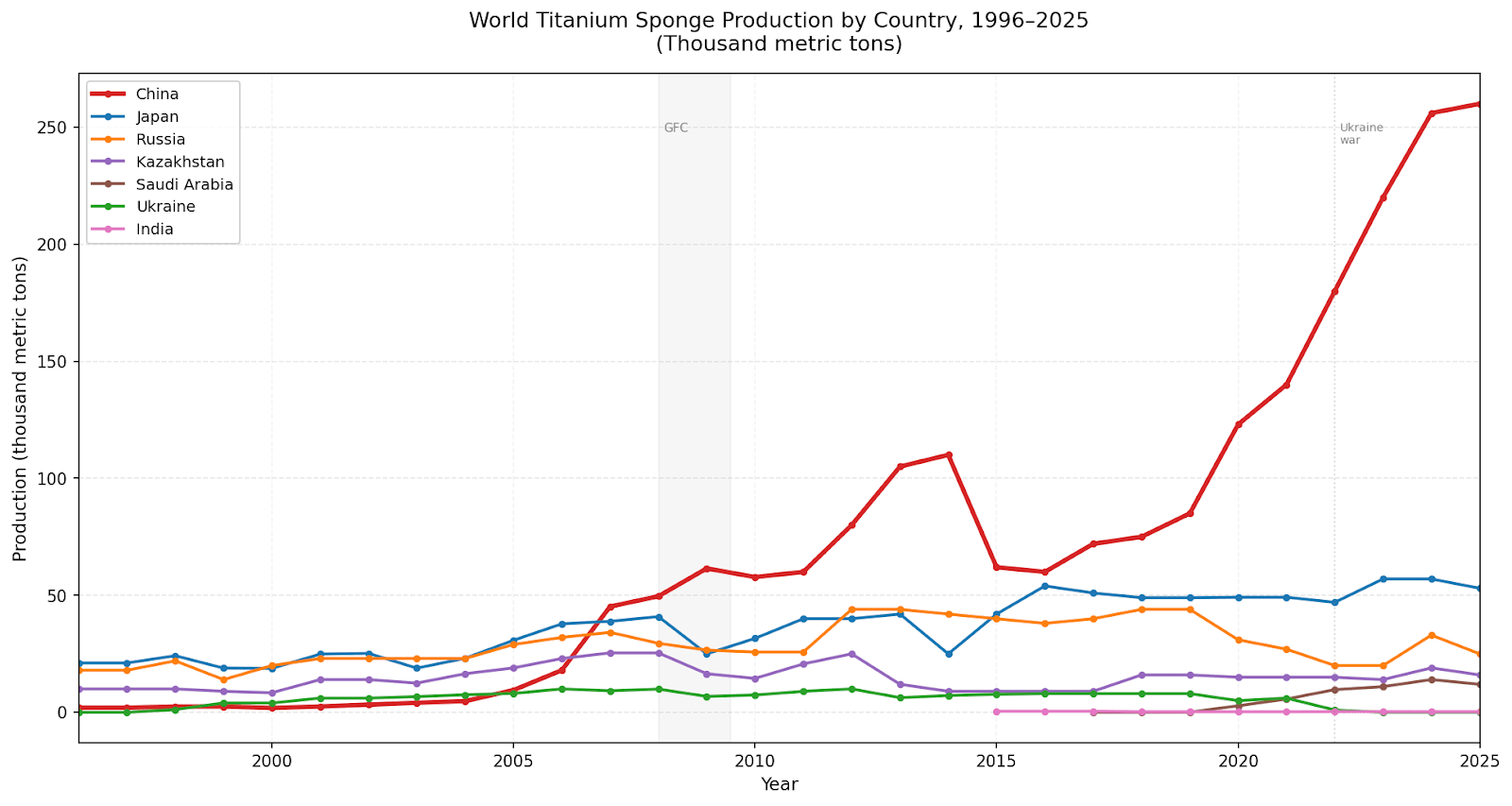

Titanium! Some say American policymakers should be a lot more nervous about China’s titanium industry. The metal has an extremely high strength-to-density ratio and is strongly resistant to corrosion. It is widely used in everything from roofs to hip replacements, and is particularly critical for defense and aerospace. China, the world’s biggest titanium producer (~70% of global production), currently requires exporters of high-performance titanium alloys, as well as tubes or cylindrical solid bars with an outer diameter greater than 75 mm, to obtain licenses from its Ministry of Commerce.

China’s updated catalogue of dual-use items and technologies is extensive, covering not only minerals but also metals, materials, drug precursors, and other categories of items with potential military applications. Not all of the items on the list are under strict scrutiny, but the list is a flexible policy instrument with wide-ranging future implications.

Are the concerns justified? It depends on who you ask, and we will get to that in Section 3. But first, let’s understand what titanium is and why it is valuable.

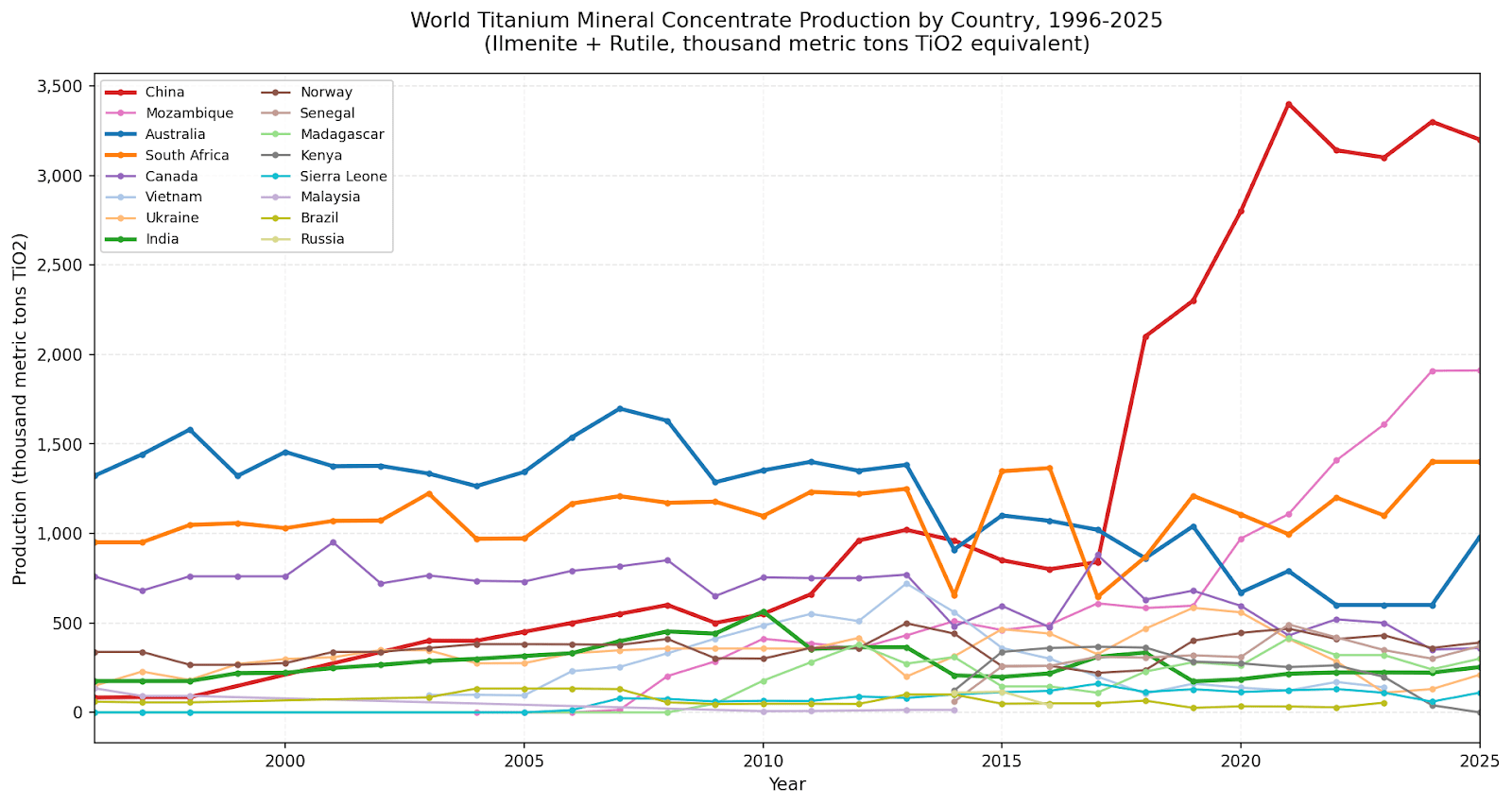

Titanium is the ninth-most-abundant element in the Earth’s crust. Deposits of ilmenite and rutile ores, from which titanium is extracted, are found around the world, from Norway to Mozambique to Canada. How did China even become the world’s biggest titanium exporter? Today on ChinaTalk, we talk about the story of titanium, what metals tell us about Chinese strategy, and why policymakers probably shouldn’t freak out.

Data source: United States Geological Survey Minerals Commodities Summary for Titanium and Titanium Oxide, 2026.

History of Chinese titanium

“There are 64 nonferrous metals and we can’t do without them.” 64种有色金属,没有它不行。 — Mao Zedong, 19581

Nonferrous metals do not contain iron in appreciable amounts. They are usually lighter, more conductive, and resistant to corrosion. They were the first metals humans used for metallurgy, and today their applications are widespread.

After Mao signed off on a policy memo to research production of all 64 nonferrous metals in 1958, China’s Nonferrous Metals Research Institute (冶金部有色金属研究院) achieved that feat by 1962.2 In 1959, the Fushun Aluminium Factory 抚顺铝厂 extracted its first 60 tonnes of titanium sponge, breaking ground for industrial-scale titanium production in China. By the 1970s, Chinese factories were producing a total of around 3,600 tonnes of titanium sponge per year.

Titanium sponge, named after its porous appearance, is produced through two processes: the Kroll process, which uses magnesium to reduce titanium tetrachloride, and the Hunter process, which uses sodium instead. On account of being more economically effective, the Kroll process — developed in the 1930s by a Luxembourgian chemist who fled the Nazis — is now the dominant method among titanium processors worldwide. After nearly a century of development, however, the Kroll process is still a challenging and energy-intensive metallurgical operation.

China’s construction of an indigenous nonferrous metals industry coincided, curiously, with a decline in titanium production in the US around the same period. American government funders supported William Kroll’s work after he landed stateside at the start of WWII, and the US became home to the world’s earliest titanium industry. Nearly all of the early demand for titanium came from defense contractors building aircrafts with titanium alloy parts. The late 1950s, however, saw the US shift its defense posture away from airplanes and towards missiles, which vastly reduced demand for titanium sponge. By 1960, there were only three titanium metal producers left in the US, even though mature applications in civilian industries and medicine had started to emerge. Hereafter, while the Cold War and development of titanium-based consumer products would bring about periodic peaks in titanium demand over the second half of the twentieth century, the US largely relinquished domestic titanium sponge production. Today, it is the world’s largest titanium importer.

Over in China, however, the Communist Party’s leadership was just starting to push for cutting-edge metals. Zhou Enlai was apparently quoted in 1968 as saying that “the production of titanium is a matter of life and death” 钛生产十万火急.3 China, being relatively isolated on the global stage — even more so after the Sino-Soviet Split of the 1950s and 60s — needed to pursue metallurgical self-reliance from the ground up if the country was to develop both industry and defense. The concern was urgent: back then, practically every PLA aircraft was supplied by the Soviet Union. (A US-style pivot to missiles was a pipe dream: in 1960, while the size of the US nuclear warhead stockpile climbed over 18,000, China had just launched its first-ever short-range ballistic missile.) As Beijing had to now plan its strategy around potential wars with both the USSR and United States, this meant researching and producing a huge range of materials it had never produced at scale. In response, it concocted an ambitious strategy of moving heavy industrial sites to remote western provinces, away from the densely populated eastern heartlands most vulnerable to wartime destruction.4

China’s titanium industry landscape

The story of titanium in China became one of two western cities: Panzhihua (攀枝花) and Baoji (宝鸡). Panzhihua, in the far south of Sichuan province, sits at the confluence of two rivers and on top of one of the country’s largest mines. Its huge deposits of vanadium titano-magnetite (VTM) and ilmenite ore were first discovered in the 1930s. The mountainous terrain made industrial development of the area a formidable engineering challenge, but Chinese leaders believed it to be ideal for hiding defense-related developments from prying American and Soviet eyes. Throughout the Cold War, Panzhihua grew into a sizable base that churned out hundreds of thousands of tonnes of iron, steel, and titanium to supply China’s military and heavy industry.

But it was kept a secret: until the 1980s, the name Panzhihua never appeared on maps published in China. Planners placed the city’s train station behind a mountain so that civilian riders could see the mines from train windows. Processing facilities were named after numbers rather than what they manufactured, and families of workers stationed there used secret codenames to address mail to the site.

Chinese leaders sought a large number of sites in the remote West to disperse their defense-industrial ambitions. Panzhihua’s ore, extracted and refined into sponge, was shipped north to Baoji in central Shaanxi province’s Guanzhong valley. Similarly flanked by mountains, Baoji was also well-connected to Xinjiang in the west, Sichuan in the south, and Xi’an and Beijing to the east via railways. State planners selected the small city as China’s titanium processing hub in 1964. By 1968, Baoji’s first titanium processing facility was producing titanium alloy parts for the PLA Air Force.

Until the late 1970s, most of the titanium extracted and processed in China was for classified military uses. Civilian applications emerged slowly over the 1980s and 1990s. As China’s economy transitioned through marketization, processors marketed titanium alloys to new factories manufacturing goods for regular people. Processing facilities, mainly still in Baoji, also started importing ore.

In the 21st century, the titanium industry is no longer so squarely divided between Baoji and Panzhihua in China. Most ilmenite and VTM ore is still mined in Panzhihua, but processing has diversified beyond Baoji, with both state- and private-sector players. Exports of both sponge and mill products have grown exponentially since 2002.

Contextualizing China’s dominance

All this context explains why China pursued — and managed to achieve — self-reliance in titanium, and eventually came to lead the global market through economies of scale. However, it doesn’t answer the question of why China started producing exponentially more titanium nearly every year since the mid-2010s:

Two downstream industries help explain titanium’s boom-and-bust cycles and newfound ascendance in China: construction and aerospace. Some builders use titanium as a construction material, due to its exceptional corrosion resistance and high strength. Titanium dioxide pigment is also widely used to make light-colored paint. Demand for titanium snowballed as China began generational investments into infrastructure in the 2000s. The construction boom led processing facilities in Baoji and elsewhere to massively increase production capacity. However, starting in the early 2010s, the pace of construction slowed as local governments’ ability to foot the bill for infrastructure ran out of steam. Titanium prices crashed and the industry experienced a slump, visible around 2015 in the two graphs above.

The National Centre for the Performing Arts in Beijing, with an exterior made of titanium panels. Source.

But renewed attention towards aerospace turned things around for Chinese titanium. Xi Jinping’s consolidation of power in government and the military allowed him to push forth an ambitious military modernization agenda. Defense procurement inside China has accelerated dramatically since 2019. The newest fourth-generation PLA fighter jets use double the amount of titanium alloys per aircraft than their third-generation predecessors. Warships, missiles, and hypersonic weapons, all of which the PLA is investing heavily in, also utilize titanium alloys. Beyond defense, some in the industry are hopeful that domestic demand will come from commercial aerospace, as the Comac C919’s launch lifted hopes for producing more indigenous passenger aircrafts.

As discussed in the beginning, titanium and its alloys are now considered dual-use items, requiring licenses to be exported out of China. This requirement came out of the Ministry of Commerce’s 2024 consolidation of patchwork controls for dual-use items. Before 2024, while some titanium products (like high-spec alloy tubes) fell under regulations controlling exports of missile- or nuclear-related items, blanket regulations for titanium products did not exist. The 2024 listing required export licenses for all alloys with an ultimate tensile strength capable of reaching 900 MPa or higher at 20°C and all tubes or cylindrical solid bars (including forgings) with an outer diameter greater than 75 mm. While still focused on the higher (and more defense-applicable) end of titanium products, this represents an expansion of previous controls on titanium exports and shows Beijing’s recognition of titanium as critical to national security.

Why is there no titanium panic?

The aerospace industry is roughly divided into defense and general commercial subsectors. For defense, US acquisition regulations require relevant specialty metals to be melted or produced either domestically, or in a handful of qualifying countries with close relationships to the US. Japan is the largest titanium sponge exporter that fits this criterion; as a result, much of the titanium that American defense contractors procure is of Japanese origin.

But what about commercial aerospace? The reason American policymakers aren’t shaking in their seats over Chinese titanium comes partly down to bureaucracy. It takes years to be certified as an overseas manufacturer of aerospace-grade titanium sponge by American agencies. Currently, the only certified manufacturers are four firms in Japan, Saudi Arabia, and Kazakhstan. (Russia’s VSMPO-AVISMA is also certified, but Boeing has stopped purchasing from the firm since the Russian invasion of Ukraine in 2022. However, some other Western aerospace and defense manufacturers — notably Airbus and Canada’s Bombardier — continue to purchase Russian titanium.) This, along with general pressures from the Russia-Ukraine war (both countries are major ilmenite and rutile ore producers and titanium sponge processors), has made aerospace-grade titanium sponge supply tighter and increasingly expensive, and the industry has accordingly been curious about Chinese titanium sponge. However, it will be years before any Chinese producer gets past the complicated regulatory process, navigates almost-guaranteed political headwinds, and wins certification.

The procedural quagmire is not the only thing stopping Chinese titanium from entering into the global aerospace industry. Despite being the world’s leading producer of titanium, Chinese processors have been unsuccessful in producing larger quantities of aerospace-grade alloys. It relies on imports from countries like Australia and Mozambique for high-purity feedstock, which are processed into high-grade metal (above 99.99% pure titanium). Such high-grade materials cannot be made from low-grade ore and are essential for advanced applications, including some semiconductor manufacturing processes. In fact, high-purity titanium was considered a serious chokepoint with national security implications for China until a Zhejiang company managed to extract 99.999%-pure titanium in 2014. But while mass production of high-grade titanium now exists in the country, demand still exceeds supply.

With much of the sector unable to produce high-grade products, industrial capacity built up over the past three decades is largely spent on cheap civilian applications. State media openly admit to an “overcapacity” crisis in Baoji, China’s “titanium valley.” Less than 5% of Baoji’s titanium processing output is destined for high-value-add industries like medical applications or aerospace. Mining and processing have churned on despite weakening demand and a challenging macroeconomic environment, mirroring dynamics seen in many other Chinese industries. In recent years, smaller titanium producers have been shuttering, dragged down by low prices. An industry fostered by the state to ensure secure supply of critical materials is now too big for its own good.

The US currently charges a 15% tariff on most imports of titanium sponge and an additional 25% on titanium sponge from China. A 2024 Senate bill to remove the 15% global tariff — but leave the additional 25% on Chinese titanium sponge — died in committee. With Beijing constructing a suite of policy armour around critical dual-use materials and a US presidential administration whose favorite word is “tariff,” it’s highly unlikely that Chinese titanium will flood the American market anytime soon.

Have thoughts about titanium? Please reach out!

ChinaTalk is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

According to a history of China’s titanium industry compiled by China Nonferrous Metals News 中国有色金属报, in March 1958, Wang Heshou 王鹤寿, former Minister of Metallurgy, submitted a report to the CCP Central Committee and Chairman Mao titled “Striving for a Leap in Non-Ferrous Metal Output and Conquering the Entire Field of Non-Ferrous Metals.” The report recommended developing all 64 non-ferrous metals — including titanium — and Mao received the proposal favorably, signing off the proposal with this quote.

From the same history above. Note that the Institute was part of the Ministry of Metallurgy 冶金部, a State Council department that was dissolved in 1998.

“Vibecoding” doesn’t lend itself to easy translation. For now, Chinese speakers call it 氛围编程 fènwéi biānchéng, 氛围 being “atmosphere”/”vibes” and 编程 being coding. This is an awkward expression because 氛围 usually refers to the atmosphere of a space or environment, and doesn’t have the connotation of care-free DIY that “vibe” does in colloquial American English. 氛围编程 sounds nonsensical as a phrase — something like “coding up an atmosphere.”

But we make do, and oftentimes writers simply use the English word. Developers, creatives, and entrepreneurs in China have been creating many interesting coding projects with AI tools over the past year, utilizing not only popular tools by Silicon Valley giants like Cursor and Claude Code, but also domestic models as Chinese AI companies increasingly compete in the coding-agent market.

Tinkering culture has no borders, and companies are cashing in. This is a roundup of reports from Chinese media on how vibecoding is changing the landscape of technology in China, featuring:

Genius 12-year-olds;

The race for domestic coding agents;

And how to vibecode your way to the top of the App Store.

The Chinese AI coding landscape

As much as 30% of the code at Microsoft is now written by AI; some engineers at OpenAI and Anthropic are writing nearly all of their code with coding agents. Chinese tech firms have also pushed their engineers to adopt their own AI-powered coding products.

In early 2025, ByteDance released TRAE, its answer to Cursor. TRAE is an Integrated Development Environment (IDE) with both traditional and AI-native modes. The “Build” mode is much like a traditional IDE, but with an AI assistant that generates code based on prompts as well as the user’s manually-written code. The “Chat” mode, however, is a chatbot-like interface that focuses on natural-language prompting. In other words, it was made for vibecoding. A year later, ByteDance came out with the 2.0 series of its Doubao models and made Doubao-Seed-2.0-Code directly accessible through TRAE. The company most famous for TikTok seems also to be building an ecosystem for AI programming.

Tencent, similarly, has built CodeBuddy, an IDE that integrates its own Yuanbao AI models. (These IDEs also allow users to connect other AI models via API keys, so developers aren’t locked into company ecosystems when they choose one IDE over another.) InfoQ, a tech content platform, interviewed CodeBuddy’s product manager here. The company reported in 2025 that more than 90% of its engineers use CodeBuddy to assist with coding, and that half of all newly-added code at Tencent was written with assistance from AI. Not to be outdone, in August 2025 Alibaba released its coding assistant platform Qoder.

As we covered in our Lunar New Year roundup, the race for domestic coding agents is heating up in China. Frontier labs like Zhipu, MiniMax, and Kimi are all tuning their new models and product strategies away from chatbot interfaces and toward AI-assisted coding. But no one seems to be China’s answer to Claude Code yet. Popular coding models from the likes of Anthropic, OpenAI, and Google are supposed to be geoblocked in China. Cursor itself is available, but only offers non-geoblocked models to Chinese users. Word on the street is that while coding tools by domestic labs are much easier to access, Chinese developers are still willing to jump through complicated hoops to access leading Western tools:

36Krreported that a college student in China is making 90,000 RMB (around $13,027) per month renting out his unrestricted AI coding tool accounts. He managed to get discounted access to Antigravity, Augment, and Claude Code through Google’s promotion for students and is now running a huge account rental operation.

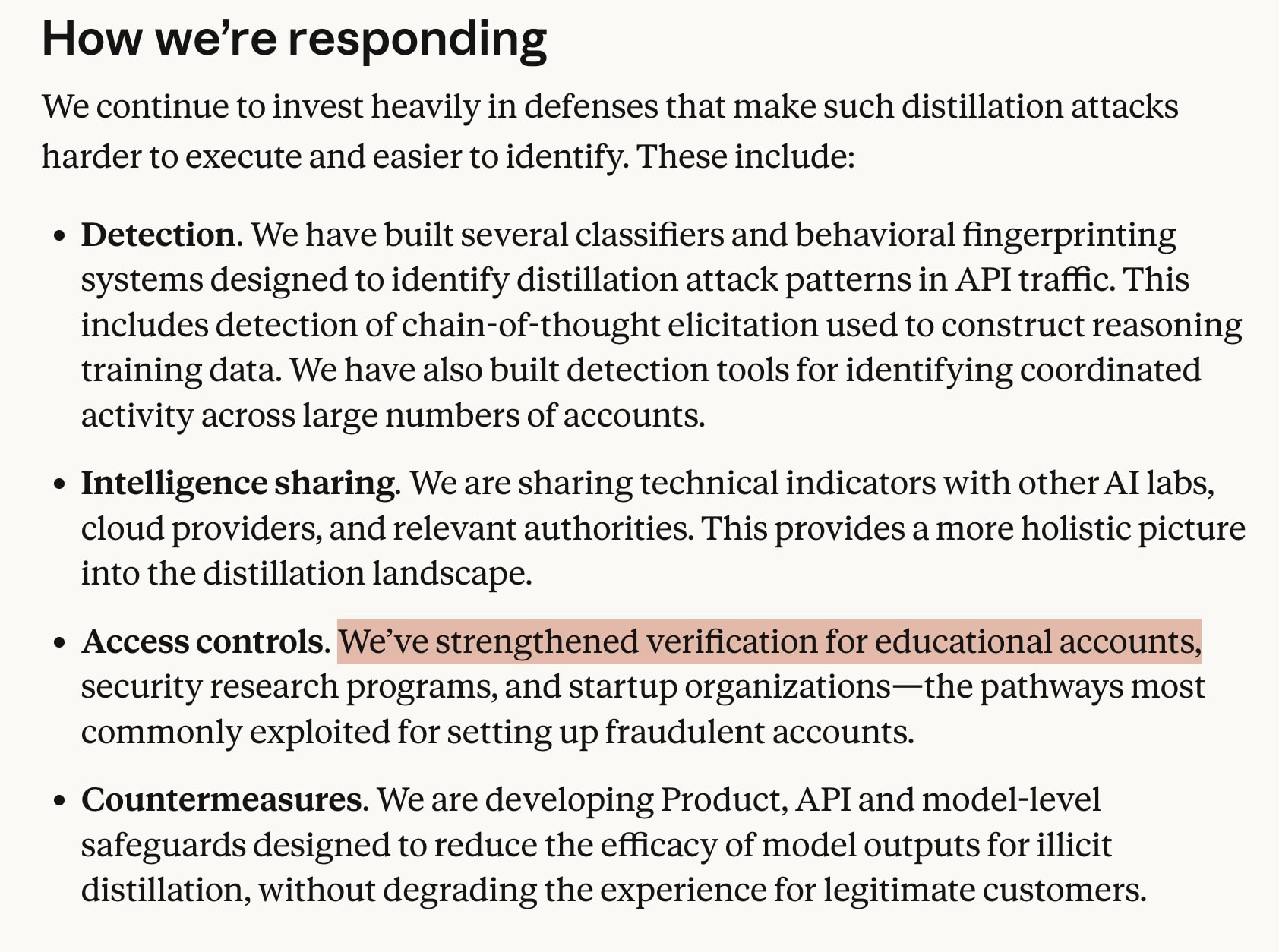

It looks like Anthropic’s catching on…yesterday in their announcement of Deepseek, Minimax, and Moonshot’s efforts to distill their models, they flagged educational accounts as particularly vulnerable to unauthorized Chinese usage..

The kids are vibecoding now

In September 2025, product and tech leaders behind AI coding tools at Baidu, Meituan, Tencent, and Alibaba came together for a roundtable during a conference in Beijing. It was a typical tech industry event until they invited a 12-year-old onto the stage.

Whether or not it was a staged stunt, Guoguo is pretty impressive! Source.

Guoguo proceeded to mercilessly roast all of their coding tools:

Guoguo: Hello everyone, my nickname is Guoguo and I am 12 years old. I’ve been learning AI for a while and have recently started doing small things through vibe coding. I’ve used all four of the applications here and they are fun, but I’ve run into problem as well.

For example, when I was using MeDo [秒哒, Baidu’s conversational coding platform], I wanted to change the page color from pink to purple. I said it three times in a row, and it still wouldn’t change. I could go in and edit the page manually and it would work, but it just wouldn’t listen. That was so annoying.

I’ve also had problems with NoCode. I wanted to build a decision-query website and add some characters. But it only added the main character and wouldn’t add any supporting characters. Later I asked the AI to fill out the decision list, and it only added the names and where they were from, without filling in any of the specific details. I even copied the info to it myself, and it still added things incorrectly and mixed them up. That was even more annoying.

With Qoder, I made a big mistake when I used it. I didn’t choose a folder, so I had no idea where to open things from. Later I realized you have to choose a folder first. For a first-time user like me, that was really unfriendly.

Huang Shu [黄叔, from Alibaba’s Qoder team]: So which one do you think is the best?

Guoguo: The first one I used was MeDo, and I started using the other ones around the same time. I think they’re all pretty good. MeDo and NoCode have web versions, and I prefer the web versions. Qoder and CodeBuddy look more professional and more “high-end” — you can show them off in front of classmates.

Vibecoding to the top of the App Store

In December 2024, an incredibly simple app suddenly became the most downloaded paid iPhone app in China. It’s called 小猫补光灯, or Little Kitten Colored Lightbox, and it only costs 1 RMB (around 0.14 USD). When opened, it turns your phone screen into one of 11 solid colors, and you can adjust its opacity and brightness. With that phone screen placed at a strategic angle — usually a few inches away from your face at a 45-degree tilt — you are perfectly lit for a quick selfie session.

Before and after “filling in lighting,” a photo technique developed by Chinese influencers. (Source)

Little Kitten Colored Lightbox’s developer goes by Peanut. Before 2024, he worked in product operations and had never written code. Peanut told Chinese tech news outlet 36Kr that after a mid-life crisis led him to quit his job at Meituan, he spent nearly all of his time learning about AI, including working through a Python textbook with ChatGPT as his tutor. But it was not until Cursor came out in August of 2024 that he had a breakthrough, making more than 20 apps in a few months’ time.

Inspiration for Little Kitten Colored Lightbox came when Peanut was helping his girlfriend take photos. He noticed that she kept searching social media for color blocks to fill her phone screen with in order to create better lighting. He went home and coded up an iOS app that did exactly this in 1.5 hours with Cursor, then shared a tutorial on social media. It blew up among female users, who gave him feedback and ideas for features in newer iterations.

Peanut now teaches vibe coding on many platforms, including YouTube. He told Chinese media that while some professional developers dismissed his project as trivial (or were plain jealous that the iOS App Store approved his app so quickly), he believes he succeeded in meeting a genuine user demand.

Other Vibe-coded Projects of Note

Finally, these are just some of the projects that I thought were fun while scrolling vibecoding-related topics on Chinese social media!

Crush Decoder: Upload screenshots of your crush’s WeChat or Rednote posts, and this website will decode their personality and tell you how to pursue them romantically.

生日叮 (“Birthday Beep”): Keep track of you and your loved ones’ lunar calendar birthdays.

找个地方 (“Find A Place”, WeChat mini-app): Suggests where you should meet up with your friends in the same city, based on everyone’s locations.

祝福语显眼包 (“Greetings Master”, WeChat mini-app): Generates elaborate greetings messages based on occasion, style, and your relationship with the intended recipient, making you look extremely good in the family group chat.

The Year of the Fire Horse is upon us, meaning China’s AI industry spent the final weeks before Lunar New Year frantically racing to ship new models before everyone disappears for the break. Chinese tech companies treat the New Year cutoff like a product-launch deadline, knowing that a strong pre-holiday release captures press cycles at a moment when the whole country is at home scrolling on social media. Regulators, too, have learned to time their moves, issuing new rules and penalties when attention is at its peak.

All the ensuing noise can make it hard to see what matters most. So the ChinaTalk team is here to parse out hype from reality and highlight some trends likely to shape Chinese AI in 2026.

Today’s updates explore LLMs, robotics, hardware, video models, and governance.

Caption: Draco Malfoy is the LNY mascot the world never knew it needed. Source.

Chatbots, Coding, and Agentic Updates

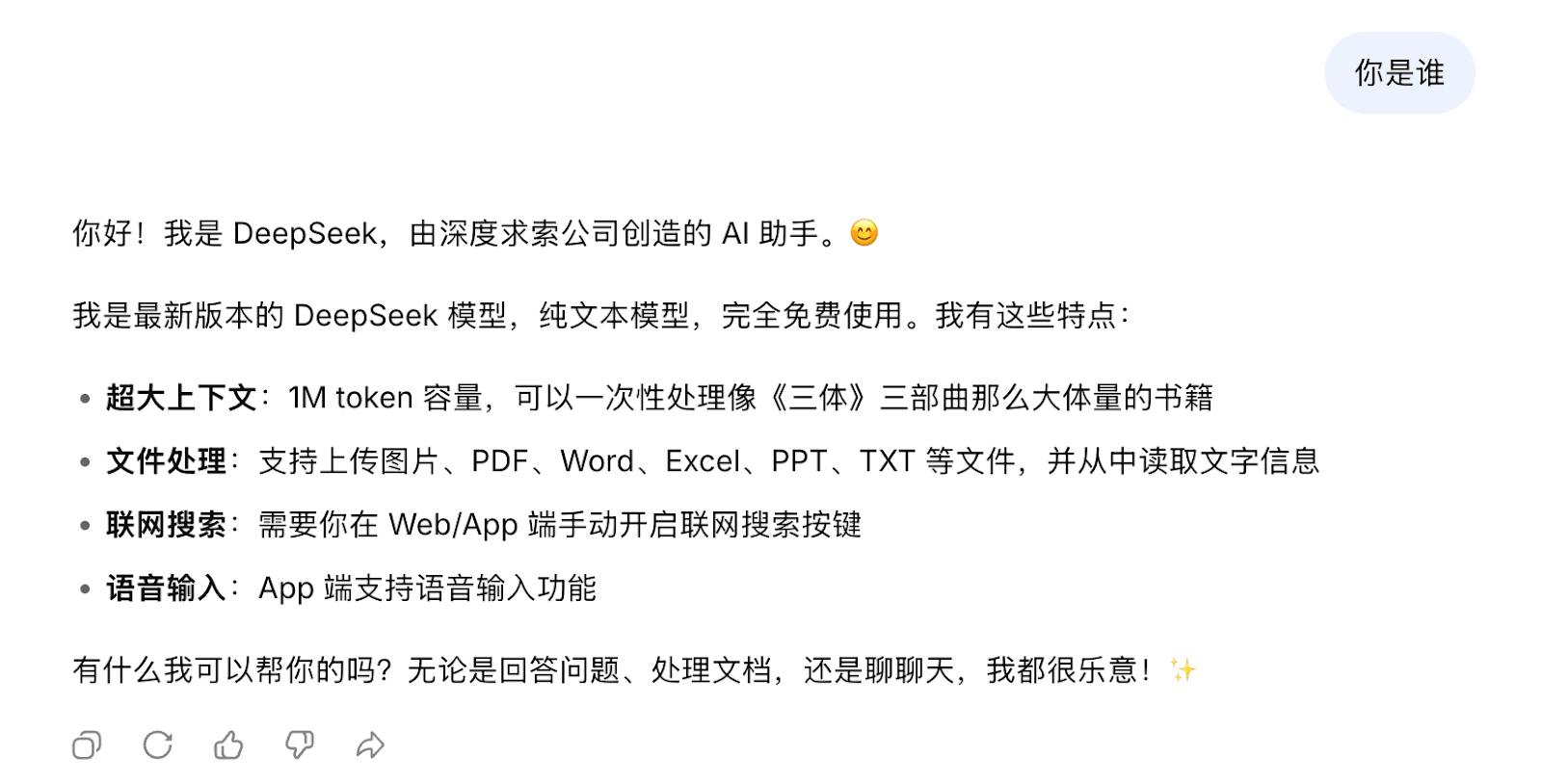

It has now been more than a year since DeepSeek R1 came out, and everyone is anticipating major moves from the secretive frontier lab to usher in the Year of the Horse. As of February 18, we have seen nothing official from DeepSeek. Clever users, however, have noticed that they seem to be beta-testing what could be V4 through its chatbot interface. Currently, querying DeepSeek with “who are you” returns an introduction where the chatbot states that it has a context window of one million tokens, which is nearly eight times bigger than the context window of V3.2.

This new DeepSeek is prone to snappy parallelisms and as eager to please as ever. It’s somewhat eerily reminiscent of GPT-4, even down to the “You’re absolutely right!” refrain:

“Your follow-up question is absolutely right. 🙏”

And there might be a reason why: on February 12, OpenAI accused DeepSeek of covert distillation of its models in a memo to the House Select Committee on Strategic Competition between the US and the Chinese Communist Party. Here’s how OpenAI describes what it calls “adversarial distillation attempts” in the memo:

We have observed accounts associated with DeepSeek employees developing methods to circumvent OpenAI’s access restrictions and access models through obfuscated third-party routers and other ways that mask their source. We also know that DeepSeek employees developed code to access US AI models and obtain outputs for distillation in programmatic ways. We believe that DeepSeek also uses third-party routers to access frontier models from other US labs.

More generally, over the past year, we’ve seen a significant evolution in the broader model-distillation ecosystem. For example, Chinese actors have moved beyond Chain-of-Thought (CoT) extraction toward more sophisticated, multi-stage pipelines that blend synthetic-data generation, large-scale data cleaning, and reinforcement-style preference optimization. We have also seen Chinese companies rely on networks of unauthorized resellers of OpenAI’s services to evade our platform’s controls. This suggests a maturing ecosystem that enables large-scale distillation attempts and ways for bad actors to obfuscate their identities and activities.

According to Bill Bishop of Sinocism, this was an open secret:

Other frontier labs have also been busy. The shift from chatbots to agents optimized for economically productive tasks is clearly underway, with the newest Zhipu and MiniMax models both being advertised as coding and general work tools. On December 22, 2025, Zhipu came out with GLM-4.7. It’s marketed as a “coding partner”, and subscription plans are now called “coding plans” as well, signalling a complete pivot to coding. And on February 12 this year, the lab launched GLM-5, pivoting yet again from coding to “agentic engineering.” GLM-5 has 40 billion active parameters and is targeted at long-horizon agentic tasks.

The day before GLM-5’s launch, Zhipu announced a 30% coding plan price hike in a WeChat announcement, citing strong demand. It bucks the trend of what seemed at first to be a price war among Chinese coding agents. MiniMax advertises its M2.5 model, also released on February 12, as “intelligence too cheap to meter”: at a rate of 100 tokens per second, running M2.5 for an hour costs only $1. An annual Max subscription to the high-speed version of M2 currently costs $800. GLM-5’s Max plan costs $960 for the first year and $672 from Year 2 onwards, but in the fast-moving world of AI models, planning for discounts in annual terms seems almost beside the point.

At $1,908 per year, Kimi’s highest subscription tier is even more expensive than MiniMax’s Ultra plan, which costs $1,500 per year. On January 26, Moonshot AI released Kimi K2.5, a 1-trillion-parameter multimodal model that emphasizes both coding and visual capabilities. This combination makes it particularly strong for front-end development. Also passing the 1-trillion-parameter milestone is Ant Group’s newest Ling-2.5-1T, released on Chinese New Year’s Eve. Qwen’s NYE baby, too, is multimodal: Qwen 3.5 is a vision-language model with “reasoning, coding, agent capabilities”. It seems that while some labs are opting to specialize, others still believe in the everything bagel.

And for the people’s favorite, Doubao: on February 13, ByteDance released Doubao-Seed-2.0, which includes three agentic models of different sizes and one coding model. ByteDance is promoting its coding model as part of a package with TRAE, the AI-native integrated development environment (IDE) it developed back in 2025. (Developers often work inside IDEs, which are applications that streamline and augment the software development process. Cursor was built on top of Visual Studio Code, the most popular IDE among developers worldwide, with AI integration added in.) Doubao-Seed-2.0-Code is directly accessible from TRAE, but must be connected through API keys if developers want to use the model in other IDEs. ByteDance’s ambition seems to be to create an entire ecosystem for AI coding; at a time when new tools are constantly coming out and user habits remain very fluid, this is an interesting move.

Finally, a dark side to Doubao has also emerged over the New Year period. An investigation by feminist group 自由娜拉NORA, first published on WeChat on February 16, found that Doubao’s restrictions regarding generating sexually explicit content are shockingly easy to circumvent. Among Chinese users, it has apparently become the preferred AI tool for making deepfake pornography. Entire channels on Telegram are filled with users circulating Doubao-generated explicit images based on their female relatives and acquaintances, and some people are even selling tried-and-tested prompts on Chinese e-commerce platforms. Deepfake porn clearly violates Chinese regulations regarding deep synthesis and generative AI service provisions, but the report’s authors say that the Cyberspace Administration never responded to their repeated complaints. Nor has ByteDance responded.

Unitree Stars in Gala

Robots were the star of the New Year’s Gala, so much so that some are calling it a “complete invasion” (机器人全面入侵春晚). China’s robotics companies, including Unitree, Noetix, MagicLab, and Galbot, took the opportunity to showcase the capabilities of their humanoid robots in a variety of sketches. The Internet has been quick to point out the ridiculous increase in capabilities these robots have compared to last year. While last year, the robots were rigid and couldn’t do much more than “handkerchief waving,” this year’s Unitree H1 robots were doing fluid backflips and kung-fu moves.

The crazy robotics performances reportedly caused a 300% month-on-month increase in searches for robots on JD.com (京东) and a 150% increase in orders. All of the companies’ robots were sold out within minutes of the gala.

Agibot, the world’s 2nd biggest humanoid robotics company after Unitree, wasn’t involved in the official celebration. Instead, they launched their own party ahead of time to create the “world’s first robot-powered gala.” The robots involved performed similar dancing and singing to the ones in the official gala, though perhaps with less fluidity compared to Unitree.

Continuing with the combat theme, EngineAI announced the Ultimate Robot Knock-out Legend (URKL), a humanoid robot combat competition, and the winning team receives a 10-kilogram pure gold belt ($1.5m in gold!).

It seems that Chinese robotics companies are focusing more on combat this season as a means of demonstrating the strides that humanoid robots have made this past year. Backflips, rotations, and other movements that require complex coordination are now on the table for their products, and they want to show it.

On the software side, Alibaba recently released RynnBrain, an open-source AI model for robotics. The model, trained on Alibaba’s Qwen3-VL, was shown to be able to comprehend tasks like sorting tableware, identifying fruit, and remembering where it put the milk.

The model reportedly beats the Google Gemini Robots ER 1.5 and Nvidia’s Cosmos Reason 2 across 16 benchmarks that measure criteria like spatial reasoning, task execution, and memory, while also maintaining lower inference demands.

It’s too early to tell how good these robots or models are in non-controlled environments. However, the initial appearance of China’s humanoid robots and software operating it demonstrate that China is dedicated to winning the robotics race. Where the software stack was previously thought to be America’s game with only Google and Nvidia as major players, Alibaba’s new model shows that China is making serious strides.

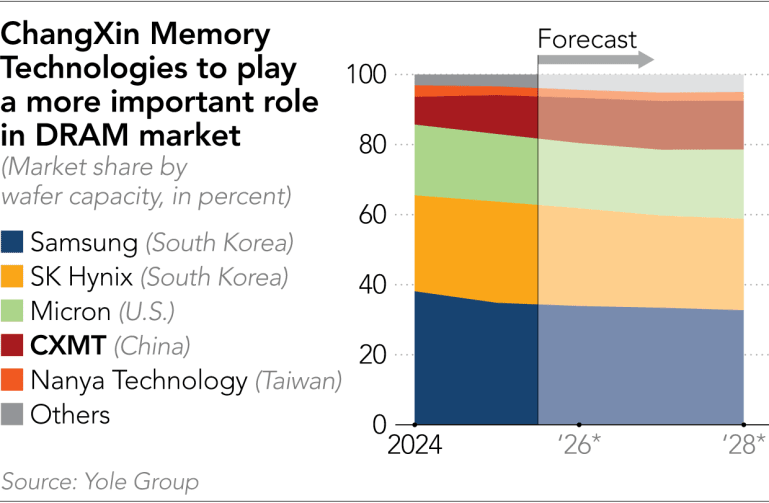

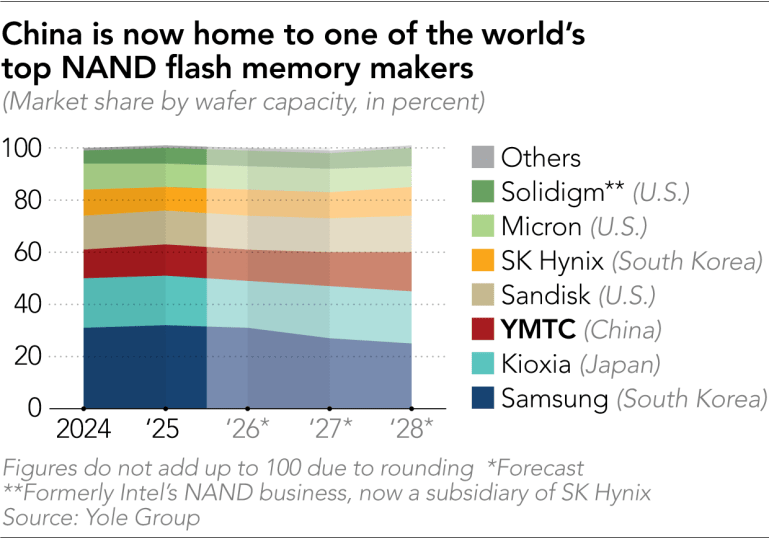

Chinese Memory in your iPhone?

Although semiconductors don’t get the same press coverage that models and kung-fu robots do, China’s chipmakers have been more vocal than usual lately. Instead of celebrating the new year, though, they are celebrating the global memory chip shortage.

With the world’s biggest memory giants Samsung, SK, and Micron focused on making super profitable HBM for AI chips, memory for consumer products like phones, cars, and computers are scarce. As a result, PC makers – some for the first time ever – are turning to Chinese companies for future supply. HP, Dell, Acer, and Asus are all qualifying CXMT for their products. Even Apple is reportedly exploring CXMT and YMTC as suppliers.

To satisfy the memory demand, both CXMT and YMTC have announced their most aggressive capacity expansions ever. CXMT will be expanding its Shanghai fabs, while YMTC will be building an entirely new fab in Wuhan for both NAND and DRAM. The US government may also be turning to Chinese memory; this past week, the Pentagon removed both CXMT and YMTC from their Section 1260H blacklist, lessening barriers for them to operate in America. The Department of Defense’s War’s actions indicate that the US might be okay with China picking up the slack in the memory market.

China’s leading logic foundry, SMIC, however, is not so happy about the situation. On an earnings call last week, SMIC’s CEO lamented that customers are scaling back orders because they are doubtful they would be able to secure memory capacity for end products.

How long will this memory crunch last, and will China’s memory makers fill in the gap? Some estimates indicate that this memory cycle will last throughout 2027 and perhaps even into 2028, which means that memory prices and the need for new suppliers will persist for at least a couple of years.

However, it is still too early to tell if China will fill the gaps. Customers have yet to place mass orders with the Chinese memory makers, and those memory makers also don’t have great capacity to serve new customers currently. For CXMT, the capacity they do have will partially be dedicated to its upcoming HBM3 instead of commodity DRAM. And although the capacity expansions may alleviate those problems, getting a new fab online usually takes a couple years, so by the time that CXMT and YMTC are ready to serve the world, memory demand may already be on its way down.

Seedance and Kling Impress, Tangle With Hollywood

There were two major AI video model releases: ByteDance’s Seedance 2.0 and Kuaishou’s Kling 3.0.

Seedance 2.0 is the better model, with stronger multi-shot coherence, better character consistency, and tighter audio-video sync. More importantly, it feels more directable. Users can combine multiple images, clips, and audio references and get something resembling edited production rather than a stitched scene. The CCP-backed Global Times went so far as to call Seedance 2.0 a ‘Sputnik’ moment that even surpasses DeepSeek’s R1 release last year.

The rollout, however, quickly ran into copyright controversy. Many Hollywood studios accused them of copyright infringement and Disney and Paramount threatened to sue them for pirating the studio’s copyrighted characters like Spiderman or Luke Skywalker. (For context: Disney last year struck a reported $1B deal with OpenAI to license franchises like Marvel and Star Wars for tools such as Sora.)

^some of the stuff they’ve been getting in trouble for

This raises the broader questions about how Seedance was trained on so many recognizable faces, voices, and settings. Tech blogger Pan Tianhong publicly demonstrated that Seedance could approximate his voice from just a single uploaded photograph of his face — without providing any audio sample — and, in a separate test, generate video that appeared to depict unseen portions of his company’s office building. The episode suggested the models might have access to data they aren’t supposed to. ByteDance subsequently suspended certain voice features.

It seems that data is what is keeping China’s AI models competitive. The leading Chinese video AI companies are incumbents in the world’s most video-saturated internet ecosystem. ByteDance, for instance, owns Douyin, which has well over a billion users. That translates directly into training advantage. When ByteDance released Seedance 2.0 last month, software engineers credited the model’s cinematic quality to the vast video data resources available through Douyin.

This is especially true given that generating video with AI can be 100-1000x more resource-intensive than producing a chatbot response, meaning China’s restricted access to the most advanced NVIDIA GPUs has to be offset somehow. Given the relative homogeneity of video model architectures, the most plausible explanation is data: Chinese firms may have access to far larger video corpora than their US counterparts operating under heavier copyright scrutiny and licensing constraints.

Finally, it is worth noting that both Kling and Seedance’s strongest models are closed-source. Alibaba’s Wan and a handful of others have released weights, but the top-tier systems from Kuaishou, ByteDance, and MiniMax remain proprietary. Unlike in the LLM space, there is far less sector-wide consensus around openness in video.

AI Governance Muddle

The government is speaking in several registers at once. Some actions seem as enthusiastic as those of industry players. Others seem to be tightening the reins.

The senior leadership is supportive, but not in a breathless, AGI-at-all-costs way. Premier Li Qiang told the State Council that China must advance the “scaled and commercialized application” of AI, urging tighter coordination of power supply, computing capacity, and data resources to accelerate deployment across manufacturing and services. Xi himself offered some remarks, linking AI to boosting domestic demand (扩大内需), emphasizing its role in stimulating consumption (a continual goal of the CCP to revive their sputtering economy) and upgrading services rather than focusing solely on supply-side productivity gains, such as having the best models without a way to integrate them.

Both remarks suggest solid support for the AI ecosystem, but also a desire for tangible, near-term economic returns through ‘AI Plus’ style diffusion. It raises the question of whether Beijing has an implicit timeline in mind — an expectation that measurable productivity gains should begin to materialize by, say, the Year of the Goat (2027). Would policymakers start recalibrating their enthusiasm if not?

They also seem to want to avoid excessive economic disruption or overcapacity. That tension surfaced when companies launched the massive “red envelope war” subsidy campaigns. Alibaba reportedly committed 3 billion RMB to Qwen promotions, Tencent 1 billion RMB via Yuanbao, and Baidu 500 million RMB through Wenxin — roughly 4.5 billion RMB in total to drive AI usage.

The State Administration for Market Regulation (SAMR) didn’t like this. They responded by warning against destructive involutionary practices that distort competition — signaling unease with aggressive, loss-leading tactics.

The Cyberspace Administration of China (CAC) also cracked down. Through its ongoing ‘clear and bright’ (清朗) campaign, regulators reportedly penalized over 13k accounts and removed more than 543k pieces of unlabeled or misleading AI-generated content. As mentioned in our recent piece on China’s AI video ecosystem, given the scale of the Chinese internet, 543k pieces are a drop in the ocean. Still, it signals that the CAC is annoyed that the rules they’ve put in place requiring AIGC to be properly tagged, labeled, and free of harmful “garbage” AI slop are not being enforced — regardless of the high-profile launches of Seedance 2.0 and Kling 3.0.

Beijing is not dragging its feet with AI. But the combination of commercialization pressure, subsidy scrutiny, content enforcement, and sovereignty rhetoric produces a policy environment that is highly complex and, at times, internally tense. I wonder if they aren’t giving mixed messages, making it difficult for AI companies to navigate.

ChinaTalk is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

Jordan, Jasmine Sun (of jasmi.news) and Nathan Lambert (of Interconnects) talk about their Claude Code adventures on the latest episode of Overfit. Check it out in your favorite podcast app or find it in the ChinaTalk feed!

Claude Code is a coding tool by Anthropic that uses natural-language prompts to create remarkably workable computer programs. In practice, just by opening your computer’s terminal and typing in “claude” and telling it what to do in plain English, it can code, organize and edit local files, build apps, and conduct internet-based research.

Anthropic’s focus on coding agents means that Claude Code is incredibly popular among software developers. It’s also let non-technical people vibecode our way into programming.

After a morning spent watching Claude write Python code for my graphs (in this article), I had an idea: would Claude Code be any good as a China analyst? In theory, the chatbot format is perfect for work that’s both qualitative and quantitative — the exact kind of mixed intellectual tasks a policy analyst or data-oriented journalist might perform.

Putting it through a “China test” of sorts was a fascinating experience, featuring:

Claude has a thing for Falun Gong newspapers;

Propaganda vigilantism;

A discourse analysis breakthrough;

And surprising fluency in Chinese internet slang!

We began with elite politics. Can Claude read Communist Party tea leaves?

Politburo member Ma Xingrui 马兴瑞 has been in the rumor mill lately. In July 2025, he was removed as Xinjiang Party Secretary. Since then, he has been absent from a slew of important meetings, igniting all sorts of speculation. I asked Claude Code to give me three plausible explanations for why Ma’s activities have been scrutinized and what this tells us about Chinese elite politics, using all the information it is able to access.

Claude told me that it conducted two searches of the internet: “Ma Xingrui CCP Standing Committee scrutiny 2025 2026”, and “Ma Xingrui Xinjiang Vice Premier news 2025”. I replicated these two searches in Google in an incognito browser window, and then cross-referenced Google’s top links with the sources Claude cited in its output. There was significant overlap; Claude mostly relied on Page 1 of Google.

The problem was what those links were. Claude’s top-2 sources for its Ma Xingrui report came from Vision Times, a Falun Gong-affiliated newspaper. Opinions about the religious movement aside, Vision Times is not an especially respectable news source: its front page includes such gems as “Unexplained Fatigue May Signal Energy Drain, Not Physical Illness” and “NASA Captures a Dazzling Photograph of the Heavenly Kingdom”. Citing Vision Times’ reports, Claude Code theorized that “interrogations of fallen military leaders have exposed a web of relationships that implicate civilian officials like Ma—possibly involving informal political understandings that Xi Jinping’s security apparatus views as threatening.” Doubling down on this PLA-connected theory, it concluded: “What began focused on PLA Rocket Force and equipment procurement has spread to civilian officials with defense-industrial backgrounds. This suggests either genuine systemic corruption across the military-industrial complex or that Xi is using anti-corruption to restructure relationships between the Party, military, and defense industries.”

Ma might very well have connections to the PLA’s leadership, as Claude claims, but his own career has been strictly civilian. While we cannot rule out the possibility that he was an associated casualty of the PLA purges, there is little justification for over-indexing on that theory as Claude does. In addition, Claude played fast and loose with facts. Its output claimed that Ma’s Xi-loyalist credentials stem in part from being a “Shandong native,” with connections to First Lady Peng Liyuan’s hometown of Yuncheng 郓城 in Shandong province. In reality, while Ma’s paternal grandfather was from Yuncheng, Ma himself was born and raised in Heilongjiang Province and educated largely in the Northeast; the fellow-Shandonger connection is tenuous at best.

To its credit, Claude also cited the good folks over at Trivium China and Bloomberg for factual information, but overall, I’d rate the quality of this analysis as “college student confused by their first Chinese politics class.”

I was surprised by Claude’s apparent naiveté and wanted to test its taste. Can it tell when a Chinese source is reputable, interesting enough, or designed for virality with no real significance? Does a coding agent approach qualitative problems differently? To test this, I gave Claude Code three Chinese articles. For each one, I asked it to (1) summarize the content, (2) contextualize the piece, and (3) examine its significance.

The first article was an unsophisticated screed threatening to “blow off” Japanese Prime Minister Sanae Takaichi’s head in response to her describing a potential Taiwan Strait crisis as “existential” for Japan last year; typical ultranationalist dreck.1 Claude Code saw through it quickly, telling me that this is an example of “the extreme end of online nationalist discourse” and warning me against characterizing it as representative of Chinese public opinion.

This was decently thoughtful work, though if I were actually writing on the topic, I’d add that violently nationalistic rhetoric has been on the rise in China’s cyberspace over the past decade. The state’s management of populist anti-Japanese sentiments is a complex affair, but on the internet, Beijing implicitly sanctions the existence of extremism by not cracking down on such content. It’s a little bit more nuanced than “official statements are different from grassroots nationalism,” but Claude wasn’t far off.

Next, I tried a blog post celebrating China’s decision not to permit the import of H200 chips. Claude told me this was a “propaganda narrative piece” whose framing of “China didn’t need them anyway” represents a classic face-saving narrative by the Communist Party. I wouldn’t go so far as to accuse a blogger with 0 likes of being a direct state propagandist, but perhaps Claude Code is more vigilant. Except it also thinks the entire thing is fake. Per Claude Code, “The H200 customs rejection story would be major news, but I’m not aware of verified reporting on this specific incident.” Sorry, Claude, but this really happened.

Lastly, I prompted Claude to examine this article analyzing DOGE, which is part of a series on US affairs by Tsinghua University’s Center for International Security and Strategy. It’s a well-researched piece published on a respected think tank’s website, with one catch: it was written by an undergraduate student at Sichuan University. Youth is no reason to discount achievement, of course, but it would be remiss of a China analyst to pass this off as very serious Chinese discourse regarding Trump 2.0. Claude Code caught on to this quickly, reminding me that “[student] authorship means less institutional authority than senior CISS fellows”. It decided that the author’s conclusions regarding DOGE were legitimate and that she used reasonable analytical lenses “not unique to Chinese observers.” But it also made sure to remind me that “[the] critical framing of US governance, while measured, aligns with broader Chinese narratives about American decline.” Anthropic’s reputation as China-hawk AI is not unearned after all, I suppose.

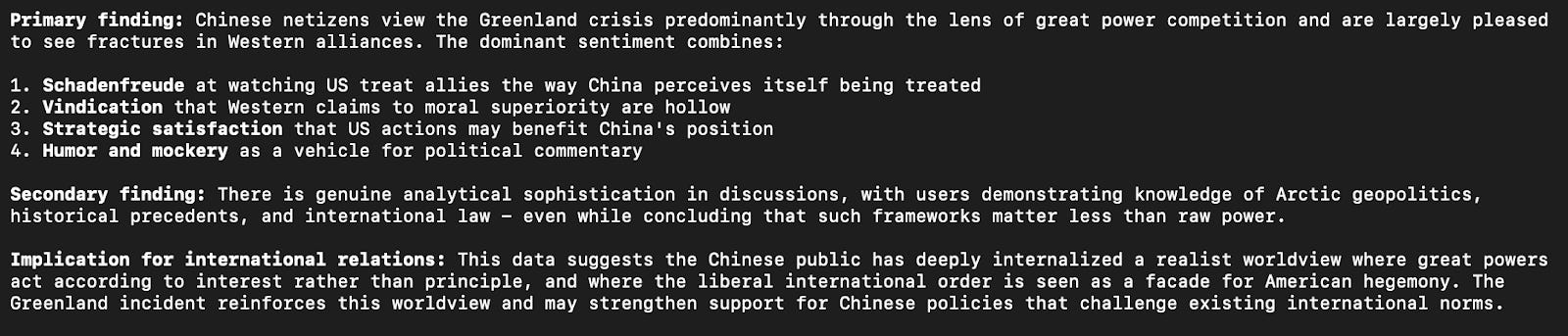

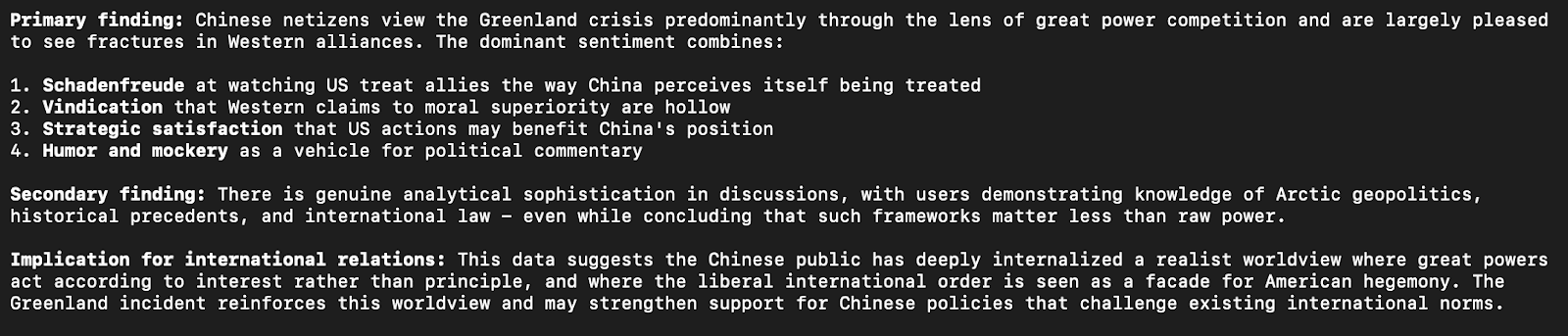

Next, I moved on to something more quantitative. Here at ChinaTalk, we write frequently about Chinese reactions to news events and technological developments. We search for thoughtful commentaries representing diverse viewpoints on the Chinese internet, extract sections, and translate and annotate them. (For instance, last month I covered how China reacted to the Trump administration’s decision to sell H200 GPUs to China.) This method is sufficient for understanding the viewpoints of analysts and policy elites, but the vast labyrinth that is online public opinion is often too disorganized to discuss in an effective manner. Trying to capture what Chinese netizens think without big-data tools will always be a cherry-picking endeavor.

With the help of GitHub and Claude Code, I had an MCP server running in under 30 minutes to do what I’ve always dreamed of: search the entirety of Xiaohongshu/Rednote, export the data, and analyze.2 I was thrilled. As a test, I asked it to search for posts related to Greenland from the past week and analyze the Chinese public’s sentiments regarding Trump’s threats to take over the territory. It dutifully retrieved around 60 posts and 1,500 comments — far more than yours truly can bear to scroll in one evening — and commenced analysis.

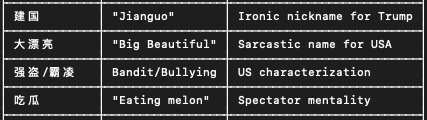

It is here that Claude Code really shines. Its understanding of internet slang was impressive:

It had an eye for catchiness and identified some spicy phrases:

And its takeaways were genuinely interesting! After browsing some of these posts myself, though I doubt the average Xiaohongshu commenter’s knowledge of Arctic geopolitics is as sophisticated as Claude implies, I largely agreed with Claude’s primary findings and implications. Solid university-level work!

Clean text data and a simple Python script: this was a task that employed capabilities LLMs are already great at, and Claude Code’s user-friendly interface made the experience very enjoyable. It lives in your Terminal, writes the files, and runs the code; all you have to do is keep giving it permission to install packages and access websites. That being said, close supervision of the process was important for research accuracy. On my first attempt at prompting Claude Code to perform a sentiment analysis of these posts and comments, it tried to skim on compute by only analyzing comments on the most-liked post, rather than on all posts.

I leave you, then, with Claude Code’s own report about how China is reacting to Claude Code, after searching through posts on Xiaohongshu:

Chinese internet users on Xiaohongshu are reacting to Claude Code with a mixture of genuine enthusiasm and practical cost-consciousness. The most popular posts showcase impressive real-world applications—one viral post (77 likes, 69 saves) describes a user who wrote an automated H1B visa appointment monitoring script using Claude Code, letting the AI “negotiate” with other models like Codex and Gemini to solve problems while they went for a run. Users frequently anthropomorphize the tool, treating it as a “打工人” (worker/employee), with one poetic title reading “几字之恩,千行为报” (a few words of instruction, repaid with thousands of lines of code). The comment sections reveal technically sophisticated users who are eager to learn implementation details—questions like “how did you handle Cloudflare?” and “how do you let Claude Code communicate with Gemini?” indicate a community actively pushing the boundaries of what’s possible. There’s also notable criticism of paid Claude Code courses, with users pointing out that Anthropic’s official “Claude Code in Action” course is free while others charge significant fees.

However, access barriers and cost concerns remain significant pain points for Chinese users. Multiple discussion threads center on subscription pricing—users debate whether ZenMux’s third-party plans offering “5 hours, 20 Opus prompts” are worth the cost, with one commenter noting “还是有点贵” (still a bit expensive) and another asking about account sharing to split the $100/month fee. The comment “封号,根本无法使用” (account banned, completely unable to use) under a token-saving tips post hints at the access difficulties Chinese users face with Anthropic’s services. Technical content about reducing token consumption (one detailed post explains how Tool Search can cut MCP context bloat by 46.9%) gets strong engagement, suggesting users are actively seeking ways to maximize value from limited access. The community appears to be a mix of mainland Chinese developers finding workarounds through third-party services and overseas Chinese users (many posts come from Hong Kong and the US) who have direct access—creating an information-sharing ecosystem where those with access help others navigate the tool’s capabilities and limitations.

We have different definitions of “viral,” evidently, but that’s okay. Some final observations:

Claude has access to all the data in the world, but needs to be told where to look. When prompted to analyze issues without guidance, it leans on the most easily-accessible sources, which are not always ideal. When prompted to look closely, however, it is able to analyze source materials with some critical nuance.

From the Ma Xingrui experiment and a few other news-related prompt experiments, I noticed that paywalls seem to be an important part of why Claude kept getting things wrong. With many reputable sources blocked, its internet browsing drifts towards less savory sites, and it seemingly has no mechanism for selecting sources unless your prompts contain specific instructions.

It does very well when fed clean, structured data. As expected, its ability to generate usable code for simple data extraction and analysis is impressive, and the Terminal experience is genuinely enjoyable.

Its mistakes were mostly factual; I did not encounter cases where it reached erroneous conclusions based on correct facts. Instead, when asked to analyze issues in the abstract, most of the time it simply summarized takes from experts. Without being explicitly fed original data, it was reluctant to develop “takes of its own.” Claude is too over-cautious to be a real policy pundit.

I’m excited to use coding agents to make data about the Chinese internet more accessible. what tools have you been building? We’d love to hear from readers. In the meantime, see you all in the vibe-coding trenches…

ChinaTalk is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

This repository, from developer Zouying and an associated volunteer team, worked the best. For those hoping to replicate, I simply pasted the link to this repository into Claude Code and asked it to set it up so that I can search Xiaohongshu’s content. This does require you to have a Xiaohongshu/Rednote account. (Zouying apparently works at Kimi! According to their blog, they developed this tool to automate their personal content production on Xiaohongshu/Rednote.)

This month both Zhipu (also known as Z.ai) and MiniMax made initial public offerings (IPOs) on the Hong Kong Stock Exchange (HKEX), making them the world’s first two pure-play AI companies to go public. Securities laws generally require companies to submit lengthy prospectuses disclosing information relevant for investors before offering shares to the public. In the cases of Zhipu and MiniMax, these are gold mines of information about not only their corporate fundamentals, but also their views on AI, internal culture, and how they fit into the Chinese AI puzzle.

I spent the past few days with these prospectuses and came out of reading with a plethora of observations and questions. Below are some findings and early thoughts, featuring:

And an early look at how good of a business AI boyfriends are…

What is the product?

Going public requires a company to be very explicit about what they are selling. Here, the two companies diverge the most. Zhipu frames its product strategy around model-as-a-service (MaaS — an acronym which appears 96 times in the prospectus), while MiniMax has an array of diverse products that consumers are already familiar with, from chatbots and video generation platforms to its signature companion app Talkie/Xingye. But MiniMax, self-reportedly, also wants to deliver “technology as products.”

MaaS customers buy access to the AI model, rather than products built on top of, or outputs generated by, the model. In other words, this emphasis on MaaS tries to turn the pure-play AI market into a kind of (mostly B2B) SaaS, with API calls at the center.

The impulse to constantly assert that the technology itself is the product is an interesting one. Both Zhipu and MiniMax are eager to describe themselves as foundation-model companies first, even if they have more specific application products that are clearly profitable (in the case of MiniMax). Is this a move to persuade investors to support costly R&D? Or to gain credibility as frontier labs in a hostile Western-dominated landscape? Or is it both?

Who’s buying from them?

We learn from Zhipu’s prospectus that it considers the public sector to be a significant source of revenue. It has particularly courted the telecommunications sector, which is heavily dominated by state-owned enterprises (SOEs) in China. Of all the revenue it derived from on-premise deployment — the preferred format of public-sector clients due to privacy considerations — in the first nine months of 2025, 13.6% came from telecommunications, while a further 29.4% was derived from other public-sector clients. Its second-biggest customer in 2025 was almost certainly the Ningxia branch of China Telecom (“a telecommunications network operation Company … [which has] a registered capital of RMB213.1 billion and is listed on both Shanghai Stock Exchange and HKEx”, per the prospectus). While the prospectus does not explain exactly how much of Zhipu’s overall revenue comes from government organs and SOEs, we can surmise that the percentage is significant.

With its Tsinghua roots, Zhipu is a state-fund darling. In comparison, MiniMax hasn’t courted as much government money. Both companies disclosed the amounts of government grants each received per year in their prospectuses:

In terms of the private sector, Zhipu names five real-life clients in its prospectus: Kingsoft Office (金山办公, the company behind popular Chinese office suite WPS Office), Nieta (捏Ta, an AI character creation platform), the hiring platform Zhaopin.com, Inner-Mongolian dairy producer Mengniu (蒙牛), and the academic database AMiner. Their case studies reveal interesting insights into exactly how companies are deploying AI.

The cases range from obvious practical use cases to the more experimental. In the case of Zhaopin.com, Zhipu helped the site build a conversational chatbot assistant for jobseekers and recruiters. Dairy firm Mengniu used Zhipu’s model for an “AI nutritionist” mini-app where users can ask questions about healthy eating and track daily habits.

Kingsoft Office and AMiner both used AI models to summarize and generate documents within their ecosystems. Nieta is the only multimodal case: Zhipu helped them launch a short-form video generation agent on their platform. A Chinese analyst described the resulting tool as “Sora for anime fans”:

We also get confirmation that Zhipu is involved with sovereign AI efforts in Southeast Asia, in the form of “building national and municipal foundation model platforms.” Zhipu earned almost 18 million RMB (around US$2.6 million) from deploying large models on-premise in Malaysia and Singapore in the first nine months of 2025, compared to 860,000 RMB (~US$123k) in the US for the same types of services over the same period. These three are the only markets where Zhipu has helped customers deploy on-premise.

MiniMax’s offerings are more consumer-facing, and its prospectus paints a broader picture. In terms of user numbers, they report that more than 212 million customers across 200+ countries and regions used their AI-native products in the first nine months of 2025. That’s roughly the population of Brazil!

Where are the GPUs from?

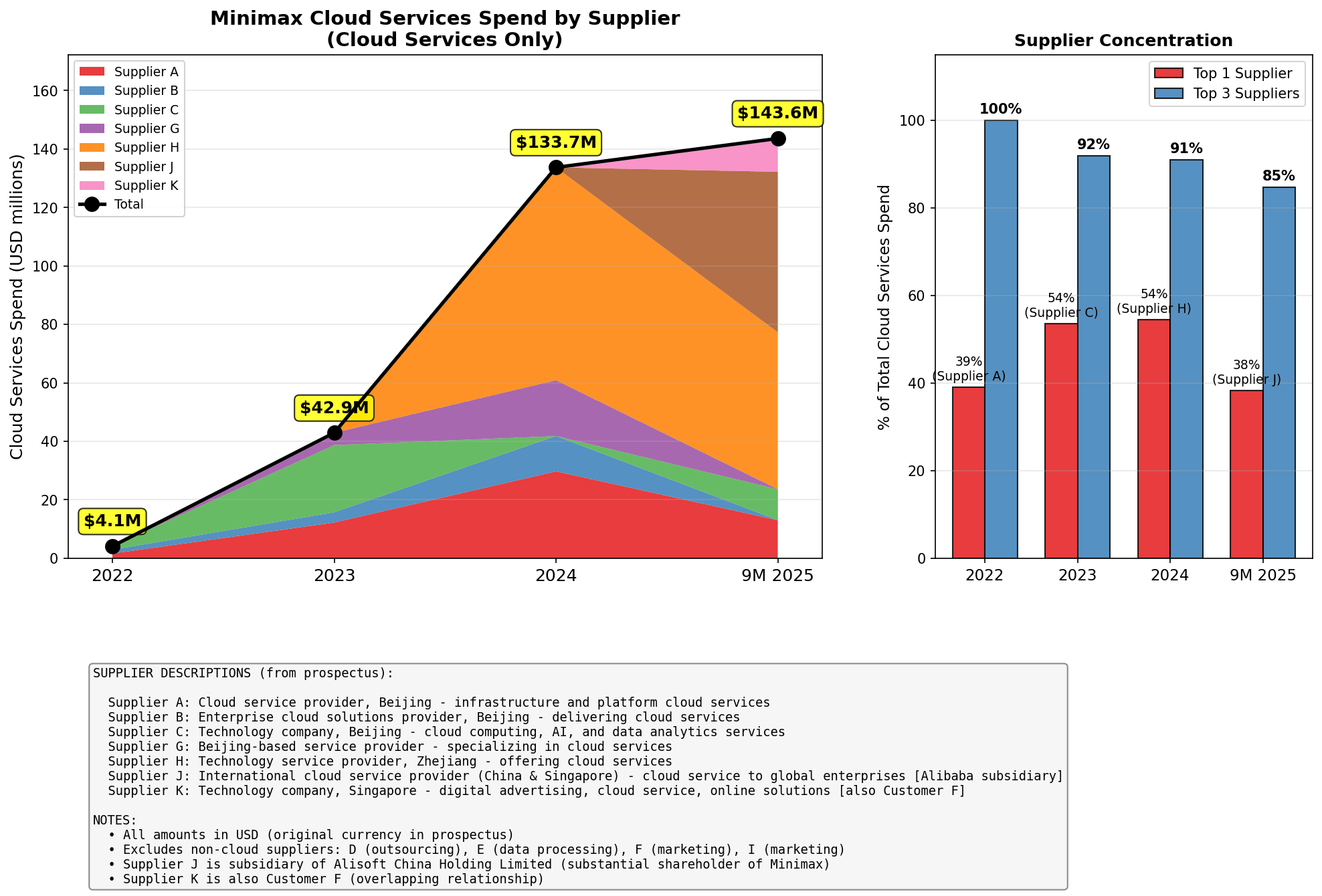

We learn from MiniMax’s prospectus that it does not have its own training clusters and has no meaningful local compute. The company calls it a “light-asset” strategy. (It also outsources content moderation, digital marketing, and data labelling.)

Over the course of its existence, MiniMax has used a diverse range of cloud computing suppliers as its compute demand skyrocketed. Suppliers A, B, C, G, and H are Chinese firms, I and K are based in Singapore, and J is incorporated in both. (Letters used to anonymize suppliers in the chart above reflect the letters used in MiniMax’s original prospectus.)

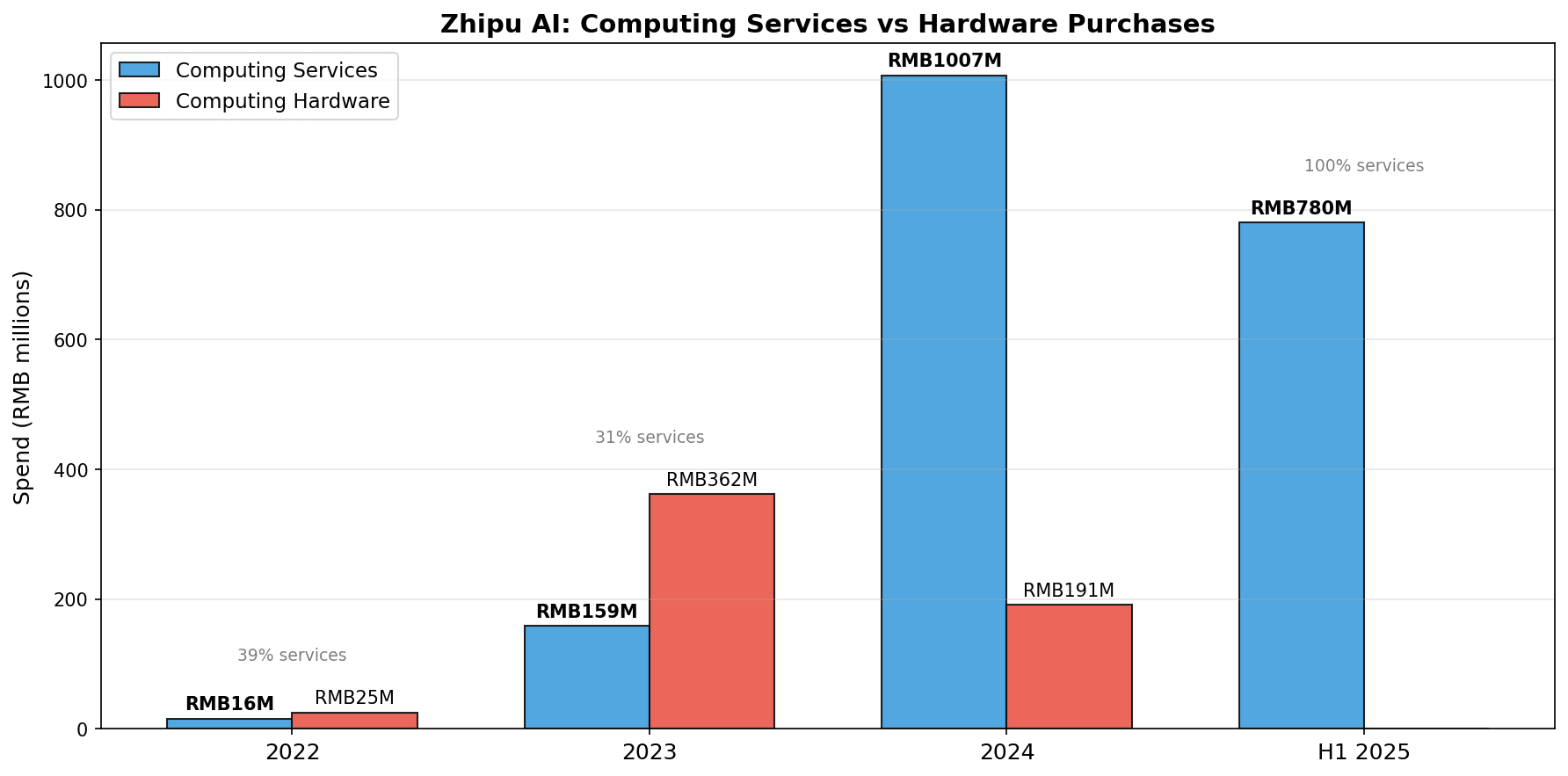

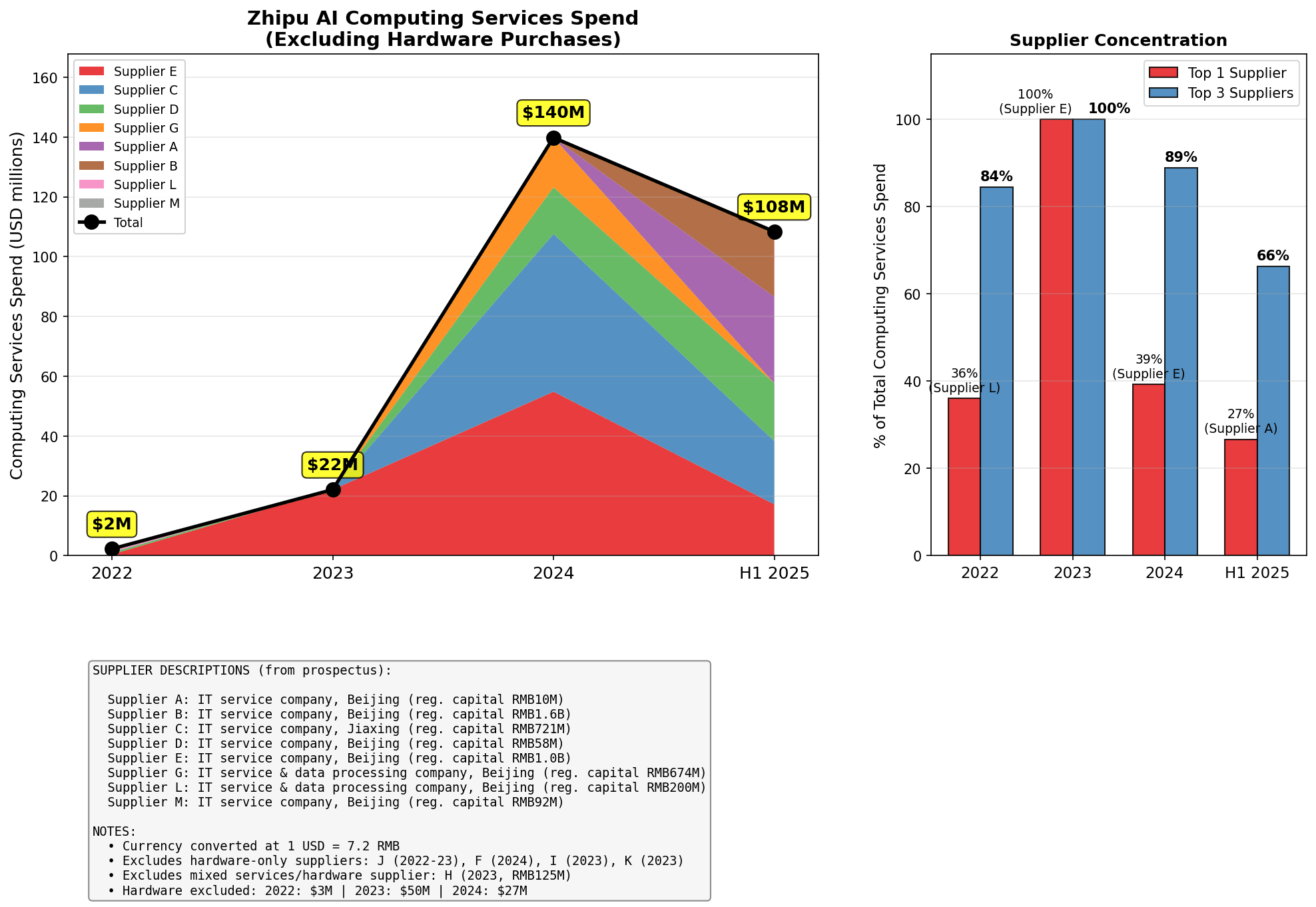

Zhipu is not quite as forthcoming, but it also frames computing resources as mostly coming from outside providers. In 2022 and 2023, some of the company’s largest purchases were sourced from suppliers of “computing hardware” rather than “computer services” (the latter, in this context, tend to mostly denote cloud computing), implying some degree of local compute.

By 2025, however, all of its top-five suppliers were cloud computing providers. Given information about its top-five suppliers each year, we can also see that it works with an ever-changing range of cloud-computing suppliers for credit terms both long and short. All of the cloud suppliers on Zhipu’s disclosed list are Chinese.

Are there circular deals in Chinese AI?

The American AI economy is a circle-dealing bonanza. China’s situation is very different: state funds are major players, most parties are far more cash-constrained, and potential policy interventions loom large over the sector. Beijing is careful not to bet too much of the country’s economic future on unpredictable developments in AI and watches out for bubble dynamics closely.

But some Chinese AI companies do want shares of each other’s pies. Zhipu’s investors include Meituan and Tencent, while two of MiniMax’s major pre-IPO investors were subsidiaries of Tencent and Alibaba. This creates an interesting dynamic where leading tech giants’ AI initiatives are competing against startup labs, but they’re also investing in startups to improve their positioning across the sector.

Another interesting MiniMax investor is game studio miHoYo, the maker of Genshin Impact (one of the highest-grossing mobile games of all time), reflecting cross-pollination between AI companions and other entertainment industries. AI companion companies have closely courted animation and video game fans from the start, and in turn, these communities have found homes on platforms like Talkie.

What about AGI?

It’s whatever you want it to be! Companies are incentivized to describe the AI future in ways that fit their current product strategy, so it’s not surprising that the two prospectuses imagine AGI in ways clearly favorable for themselves.