How China's Preparing for the Next Pandemic

Most coverage of China’s pandemic response has focused on its handling of COVID. Far less attention has been paid to what China has done in its aftermath, during which the country has been making interesting moves to prepare for the next large-scale biological threat.

Since 2023, Beijing has revised the Infectious Disease Law (IDL) and the Biosecurity Law and launched new frameworks like the Public Health Emergency Response Law (PHERL). Their rhetoric has also been increasingly telling, with criticism of the US’s pandemic response and self-proclamations of China as a global leader in pandemic oversight.

Pandemic prevention in China has moved from emergency reaction to long-term system design.

Chinese officials appear determined to ensure the next COVID doesn’t start within their borders. That determination increasingly stands in contrast to the United States, where public health institutional capacity has lost steam since 2020, especially during Trump 2.0.

Today’s installment examines governance initiatives, but this is only one part of a much larger ecosystem. Future pieces hope to explore PPE stockpiles, vaccine production, early-warning surveillance, research and lab standards, and the AI-bio crossover.

Main Takeaways

The CCP looks to be taking pandemic risk seriously. After China’s public-health system was shown unfit for purpose when COVID hit, Beijing has now enacted some of the most actionable steps of any major country to bolster its pandemic-readiness system.

COVID exposed how costly Beijing’s old instincts were: burying early signals, punishing whistleblowers, and relying on improvised crackdowns left the center blind and politically exposed. The new reforms try to fix this by giving local officials clearer rules, reporting guidelines, and more room to act early without fear of punishment. Beijing appears willing to trade some information-control for a more rule-bound, faster-moving system, though whether officials feel empowered to speak up remains uncertain.

A more centralized domestic monitoring and command system gives China greater ability to manage potential outbreaks internally, reducing pressure to depend on international organizations. That avoids reputational costs and protects “face,” which helps explain why China can buy-in heavily to pandemic preparedness while still resisting meaningful collaboration or data sharing with groups like the WHO.

Globally, Chinese state rhetoric casts the U.S. as the country that bungled COVID while downplaying its own early missteps. And Beijing is positioning itself as an international leader on health governance, especially for the Global South.

*Starting with “Recent Government Initiatives,” each section ends with a grade. Taken together, China earns a C+ overall, which is an improvement over the D I would have given it pre-COVID, though still shy of the B- I’d give the US.

Roadmap of China’s Agencies

Since 2023, the major players in China’s pandemic readiness system have received new mandates, budgets, or planning documents to strengthen their roles.

At a high level, China’s system runs on a clear hierarchy. The State Council directs national strategy, the National Health Commission (NHC) leads implementation, and a network of technical and support agencies (at both federal and provincial levels) executes the work.

Key Players

State Council (国务院) — the top command centre in any outbreak. It activates the “Joint Prevention and Control Mechanism” (联防联控机制), created during COVID, to coordinate ministries across health, industry, and emergency management. Since 2023, the State Council has signalled an effort to bolster its coordinating role for pandemic response.

National Health Commission (国家卫健委, NHC) — China’s main health authority and a cabinet-level executive department of the State Council. It drafts and enforces key laws, oversees the China CDC and the National Health Emergency Response Center, and manages early-warning and emergency-medical systems.

National Administration of Disease Control and Prevention (国家疾控局, NADC) — created in 2021 to strengthen disease control and biosafety. It sets national standards for surveillance and builds modern early-warning/data systems. It’s one of the key additions of China’s post-COVID infrastructure.

China CDC(中国疾控中心) — the technical core of the system. It collects and analyzes infectious disease data, runs testing labs, and provides guidance to local CDCs. The CDC workforce numbers surged during COVID, increasing by about 20% to reach 240,000 in 2022, the highest level ever. This was preceded by years of post-SARS neglect, which left the system understaffed and unprepared for COVID (see graph below).

There are also many supporting ministries that handle logistics, funding, and research, such as

National Health Emergency Response Center (国家卫生应急中心) - coordinates emergency medical teams and logistics during crises.

National Biosecurity Work Coordination Mechanism (国家生物安全工作协调机制) - coordinates biosecurity-specific policy and emergency response across ministries.

Ministry of Industry and Information Technology (工业和信息化部, MIIT) - manages medical supply production and logistics.

Ministry of Science and Technology (科学技术部, MOST) - supports new R&D programs in pathogen detection and modelling.

National Medical Products Administration (国家药品监督管理局, NMPA) - fast-tracks new countermeasures.

People’s Liberation Army (中国人民解放军, PLA) - deploys medical units and runs military R&D in pandemic-related situations.

How Does the US Compare?

In China, authority flows from the State Council through the National Health Commission and its affiliated agencies. Provinces largely mirror this structure, which makes it easier to coordinate and implement national policy quickly once priorities are set in Beijing.

The US system is much less centralized. The Department of Health and Human Services — mainly through the CDC and the Administration for Strategic Preparedness and Response (ASPR) — leads at the federal level, but state and local governments hold most of the practical authority over public health measures. In practice, the federal government provides funding, guidance, and aggregates data, yet in a major pandemic, it’s less clear that the US could quickly coordinate a unified national response.

Centralization, on the other hand, has trade-offs. China’s unified chain of command can move quickly, but a bad call at the top can misdirect the entire system. The U.S.’s decentralized model is more heterogeneous, since one state’s mistakes don’t necessarily drag everyone else down. China’s approach, therefore, relies heavily on accurate information flowing upward and on giving localities enough room to adapt policies to local conditions, which many of the initiatives below attempt to do.

Recent Government Initiatives

In September 2025, China’s top legislature (NPCSC seventeenth session) passed the Public Health Emergency Response Law (突发公共卫生事件应对法, PHERL). It’s the country’s most significant effort since COVID-19 to overhaul how it manages outbreaks, arriving alongside a substantial revision of the Infectious Disease Law (传染病防治法, IDL) earlier this year. Together, the two laws do a good job of weaving in many of the major pandemic readiness updates in recent years, and are meant to give China a more coordinated and legally coherent framework for handling future epidemics.1

One surprising feature of both PHERL and IDL is that neither substantively mentions the Biosecurity Law (生物安全法). Since its introduction in 2020/2021, the Biosecurity Law has been China’s main legal framework for managing biological risks, specifically, from pathogen labs to zoonotic disease surveillance. The law divides biotechnology research and development activities into three risk categories — high, medium, and low — requiring approval for high-risk and medium-risk activities. It also establishes classified management of pathogenic microorganisms and hierarchical administration of pathogenic microorganism laboratories. The law was mildly amended in 2024, though many of its weak spots remain.

The gist of these recent moves is an attempt to correct the legal and regulatory weaknesses that became apparent during COVID. At the time, SARS-CoV-2 was classified too slowly, lines of authority in emergencies were poorly defined, and rigid central control over information disclosure left local governments hesitant to act.

All Talk?

Do these reforms have any teeth? There are a few ways to parse this out.

The Biosecurity Law, IDL, and PHERL are binding laws (法律) passed by the NPC Standing Committee. This makes them more authoritative than the guiding opinions (指导意见) and plans (方案) that often crowd China’s policy space. Responsibility for their implementation also increasingly falls under the State Council, the top executive body of the land, giving these measures more political backing than if they were purely the responsibility of various lower-ranking ministries.

Still, the NPC passes many laws that aren’t effective. This is because (1) people don’t know they exist, or (2) they are not clear enough to be actionable. Therefore, what’s more important is enforcement clarity. Can local officials, hospitals, and labs actually understand what these laws require and act on them in real time? Here, the picture is mixed.

Many provisions are more explicit than previous drafts, but some remain vague or lack operational detail. For example, Article 74 of the IDL allows private entities to file complaints (申诉) if they believe emergency measures are excessive, a gesture to remediate the lack of voice many people felt during Zero-COVID. However, Article 74 offers little guidance on how such complaints will be handled or whether they provide meaningful recourse, making it unclear to people tempted to complain whether they will face consequences. By contrast, more fleshed-out stipulations like the updated early-reporting requirements (explained in the next section) clearly spell out responsibilities, timelines, and penalties, making them more obviously enforceable.

After reviewing the earlier versions of the IDL and Biosecurity Law and comparing them with the updated texts and the addition of PHERL, the system as a whole has gained some enforcement clarity. My rough sense is that only about 20–30% of the original provisions felt truly actionable, meaning that, as a local official or doctor, you could read them and understand what you were expected to do. In their current form, it feels closer to 40%.

Enforceability is jagged, though. The revised Biosecurity Law doesn’t feel meaningfully clearer to me, while PHERL and IDL seem to have made big strides.

Finally, we can look to historical analogues. The post-SARS reforms significantly reshaped China’s pandemic response system. Before 2003, the public health apparatus was fragmented and underfunded; the China CDC had only been established a year before, and case reports were still handwritten and faxed to Beijing. SARS prompted the government to carry out a wave of initiatives, such as building a real-time reporting network that linked clinics and hospitals across the country. The SARS reforms were incomplete, of course, given China’s lack of preparation for COVID, but it was a significant evolution from what little previously existed. The post-COVID reform wave feels like a similar energy stemming from a similar realization that their pandemic readiness system was far behind where it should have been.

The Content

*Graded from Best to Worst: Partly Post-COVID Improvements, Partly Overall Performance

Interagency Coordination

PHERL and IDL stress interagency coordination. The “joint prevention and control mechanism” (联防联控机制) created by the State Council during COVID is now written into law. It brings together more than 30 ministries and agencies across health, industry, and emergency management. At least a dozen civilian and military departments must share surveillance data, coordinate logistics, and build a unified national information platform for early warning. The aim is to keep ministries from working in silos and ensure outbreaks are met with synchronized mobilization.

Before COVID, no comparable command structure existed. Outbreak response rested with the NHC and China CDC, agencies without the authority to pull in heavyweight ministries or compel timely reporting from local governments. Coordination was improvised and slow. By placing the joint mechanism under the State Council, PHERL and the IDL give epidemic response a body that can enforce nationwide logistics and require all relevant ministries and provinces to report upward, ensuring that at least one institution has a complete, real-time picture of the entire situation.

Grade: A-

Mobilizing dozens of ministries and a national response is something the CCP can do better than anyone. The key caution is avoiding excessive uniformity; provincial conditions vary, and a highly centralized system must take care not to impose directives that could overlook unique situational circumstances.

Classification

The IDL updates China’s three-tier disease classification system (Classes A, B, C). Class A diseases, such as plague and cholera, trigger the highest-level emergency responses: immediate reporting, mandatory isolation, and broad quarantine powers. Class B diseases, like SARS or COVID (once it was officially listed), require strong but somewhat less sweeping interventions. Class C diseases, being the least concerning, are monitored primarily for trends and local containment, such as influenza or the mumps.

Previously, new or unknown pathogens couldn’t trigger a response until they were formally classified, a flaw made clear by how long it took to classify COVID. The revision tries to fix this by adding “sudden outbreaks of unknown origin [突发原因不明的传染病]” as an event that can be treated as Class A for response purposes. This designation prompts the State Council to rapidly investigate and issue a formal recommendation, allowing containment measures to begin before full classification is complete.

The concern for diseases of unknown origin reflects China’s growing rhetorical emphasis on “Disease X (X疾病)” (coined by the WHO in 2018), which calls for proactive preparation against future, as-yet-unidentified pathogens. As a government white paper put it earlier this year, China now aims to “draw on the experience of COVID-19 prevention and control, and make proactive preparations for future pandemics such as Disease X.”

Grade: A-

This lets officials act preemptively rather than reactively, but I’m docking half a grade as the incentives around sounding the alarm early are still uncertain. It’s unclear whether people will actually feel safe triggering a potential Class A response even when they’re technically allowed to do so.

Monitoring and Surveillance

Surveillance has taken on a more prominent role in the new framework. IDL Article 42 now mandates what’s called “sentinel surveillance” (哨点监测), a system in which selected hospitals and clinics continuously report data on specific diseases or symptoms to detect unusual spikes early. The revisions also strengthen requirements for identifying and reporting clusters of unknown or emerging illnesses, bringing China’s procedures more in line with the World Health Organization’s revised International Health Regulations (IHR).

Article 13 forbids excessive data collection and limits the use of personal information (like digital travel codes) to infectious-disease prevention and control. In theory, that’s a privacy safeguard; in practice, it’s anyone’s guess how strictly those boundaries will be enforced.

More speculatively, China’s ‘AI Plus’ Plan and related AI + Medical/Healthcare guidelines envision using artificial intelligence to enhance this surveillance network. The health-industry guideline lists public health services as one of four key application areas for AI, and pilot programs in cities like Shanghai are experimenting with AI systems that use citizens’ health data for lifelong health monitoring or proactive symptom detection. These efforts, however, remain largely aspirational.

Grade: B+

China already has the world’s most capable general surveillance system, so it will likely be able to implement this effectively. It’s still surprising that disease-specific surveillance measures weren’t firmly in place before COVID.

Local Authority

Under the IDL, local authority is also expanded. County- and city-level governments can now issue early warnings (Arts. 9, 53) and activate emergency responses when dealing with a sudden outbreak of unknown origin (Art. 65). This aligns the IDL with the Emergency Response Law, closing the gap between local initiative and national oversight. In theory, it allows quicker reaction on the ground while keeping reporting lines to Beijing intact.

Grade: B

Local officials can now move faster while Beijing deliberates — just not too fast, given an early move might look bad optically and provoke backlash from Beijing if it turns out to be a false alarm, given how vague the ostensible protections are.

Government Accountability

When it comes to checking central government power after some of the most controversial Zero-COVID measures — such as sealing residents in their homes, welding apartment doors shut, mass quarantine transfers, and imposing citywide lockdowns that lasted weeks — the recent reforms offer only modest adjustments. New provisions require local governments to ensure food and water supplies, maintain medical access, protect vulnerable groups, publish emergency hotlines, and keep workers employed during lockdowns (Arts. 64–67).

These steps are intended to prevent the worst excesses, but they do not meaningfully limit the state’s authority to impose sweeping restrictions in the first place. It is stated multiple times that decision-making remains centralized, and local officials must still carry out whatever directives Beijing issues.

Grade: B-

The CCP won’t be publicly apologizing for Zero-COVID anytime soon. But these reforms tacitly acknowledge its excesses and theoretically prevent future worst practices, like quarantined residents being locked in their homes without food.

Punishment

The revisions further strengthen enforcement but aim to channel it through clear legal authority. Individuals or institutions that refuse to cooperate with legitimate disease-control orders can now face fines of up to 1,000 yuan (~US$140), and entities up to 20,000 yuan (~US$2,810) (Art. 111 of IDL). Previously, Chinese law didn’t penalize most violations of epidemic orders, forcing police to repurpose unrelated statutes — such as those meant for constitutional “states of emergency” — to enforce zero-COVID restrictions. The fine is small, but “refusing to cooperate” is defined so broadly that even something like declining to wear a face mask could trigger a penalty.

Grade: C+

If this were aimed at punishing officials who bury crucial information — like those in Wuhan who hid early COVID signals — it would be a big upgrade. Instead, it mostly adds small fines that feel more suited to policing minor noncompliance, which risks echoing the punitive instincts of Zero-COVID rather than fixing the real failures.

Dual-Use Technologies

The Regulations on the Export Control of Dual-Use Items (中华人民共和国出口管制法), updated in late 2024, fold biological materials, technologies, and associated equipment into the same export-control framework that governs chemical, nuclear, and other sensitive goods. Under the new update, biological exports are managed through MOFCOM, under the State Council, which now appears to have greater authority over licensing and enforcement. Still, it’s unclear what exactly has changed — the specific list of what qualifies as “dual-use” biological items has yet to be clearly defined.2

Grade: C

This feels more about restricting what China sells abroad than about tightening its own safeguards around creating dual-use biological tools to begin with. It’s good as a nonproliferation measure, but the issue of creating clear research norms and controls over dual-use work inside China is still largely unaddressed.

Early Reporting

A core reform is early reporting. Under IDL, hospitals, blood banks, and local CDCs must report suspected outbreaks, clusters of unknown illness, or abnormal health events within two hours through the national Direct Reporting System. Those who report in good faith are protected from punishment (and eligible for some sort of award) even if their alerts later turn out to be wrong (Art. 51), while any official or institution that interferes with or delays reporting can now be penalized.

These provisions appear to respond directly to the early weeks of COVID-19, when local officials in Hubei delayed or suppressed information about the emerging virus — most infamously in the case of Dr. Li Wenliang, the Wuhan physician reprimanded by police for spreading “false information” after trying to warn colleagues about an unusual respiratory illness. Tragically, he later died from COVID.

However, it’s never really explained what disease reporting is supposed to include, and the promise of protection for “good-faith” reporting also feels fuzzy, since no one has defined what counts as good faith.

Grade: C-

If I were a doctor, I’d still be somewhat uneasy reporting early warnings. The protections are vague, and the precedent for punishment is much higher than in other countries.

Biotechnology Risks

The biggest shortcoming with China’s pandemic readiness system, in my opinion, is that it has not made substantial progress in addressing the safety risks posed by biotechnology — meaning the dangers that arise when genetic engineering, synthetic biology, or laboratory manipulation of organisms could unintentionally create or amplify biological threats.

The 2021 Biosecurity Law was the first statute that gestures at governance in this space. It formally divided biotechnology R&D into three risk tiers — high, medium, and low — with high- and medium-risk projects requiring approval or registration and restricted to legally incorporated domestic entities. The law also established security management rules for human genetic resources and biological resources.

The law was amended with updates that took effect in April 2024, but the changes appear largely procedural rather than substantive. There are still no specific ethical guidelines for biotechnology R&D; the three-tier risk system (high, medium, low) lacks concrete criteria for how projects should be classified; and the vague references to “relevant departments” (有关部门) leave unclear which agencies are responsible for what. In practice, this means ethical oversight is likely to devolve to institutional review boards or ministry-level discretion. These bodies vary widely in capacity, and because biotech research is competitive, institutions may have incentives to adopt more permissive review practices to maintain an edge.

This gap is likely related to the fact that Beijing also views biotechnology as a strategic growth sector. Much of the Biosecurity Law reads more like a biotech development agenda with biosecurity sprinkled on top. Article 5, for instance:

“The state shall encourage innovation in biotechnology, strengthen the building of biosecurity infrastructure and the biotechnology workforce, support the development of the bioindustry, raise the level of biotechnology through innovation, and enhance the capabilities to guarantee biosecurity.”

Grade: D

Synthetic pathogens are one of the most plausible routes to a truly catastrophic outbreak, yet Beijing’s biotech push largely ignores these safety concerns. However, in the US and other countries, ethical oversight also seems to fall to institutional review boards or ministry-level discretion, so I can’t give this a completely failing grade.

To sum up, China’s recent policy initiatives reflect a system trying to learn from its own COVID contradictions. Beijing wants a more unified and legally codified pandemic readiness system, one that detects and contains outbreaks before they spread, but also one that avoids repeating harsh crackdowns and which made provincial authorities feel powerless to national authorities. It’s a tough balance to strike.

Overall Grade: C+

Many of the laws and local incentives are still unclear, but Beijing is at least increasingly turning abstract goals into concrete procedures and has an unmatched capacity to trigger a unified response. And unlike some countries, its rhetoric does not actively denigrate public health measures.

For reference, I would give the US a B-. Even with its issues, the US does better at dual-use tech governance [pdf] and has better incentives for early reporting and information sharing.

Funding

Funding is an indicator of whether these statements have backing to them, but data is limited.

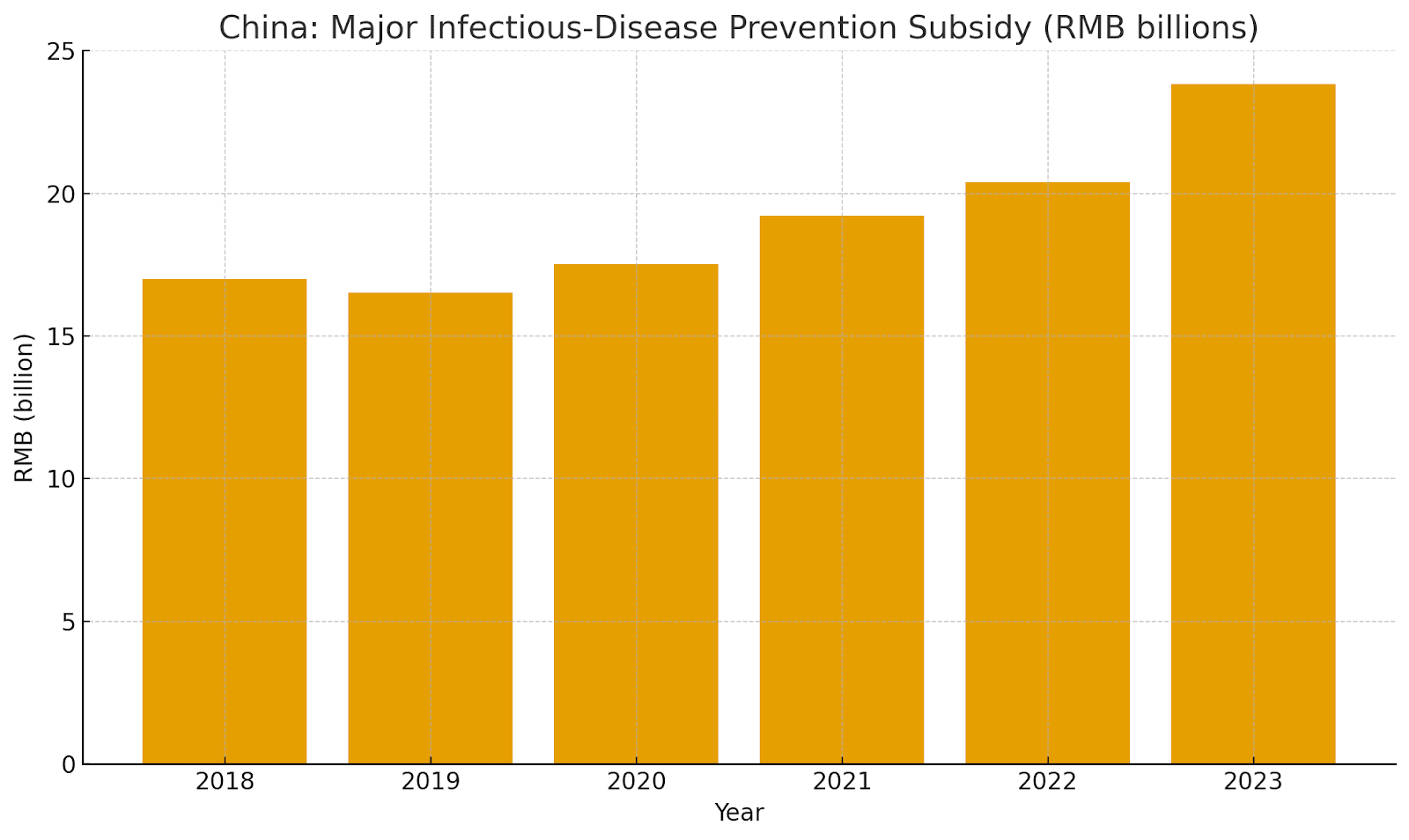

Our best piece of evidence comes from the Chinese Ministry of Finance, which shows that major infectious-disease prevention funding rose from about ¥16.98 billion ($2.38 billion) in 2018 to ¥23.82 billion ($3.34 billion) in 2023 — an increase of roughly 40% over five years. These funds are meant to expand things like vaccine-production capacity, surveillance systems, and hospital preparedness.

There’s no visible COVID-era spike in 2020–21 because much of that emergency spending flowed through temporary epidemic-response channels — one-off MOF transfers and provincial emergency budgets — rather than this regular subsidy line. The subsidies in the graph instead indicate Beijing’s effort to institutionalize emergency spending within its normal public-health budget.

Small bits of additional evidence tentatively point in the same direction. China launched a multi-billion-dollar reconstruction of the national CDC system in 2023, alongside major provincial investments in places like Shanghai and Guangdong. Data beyond 2023, however, is limited, so drawing further conclusions would be premature.

Grade: B-

They’re on an upward trend, but the total still looks modest relative to China’s GDP and population. In 2023, ¥23.8 billion (~US$3.3 billion) works out to only about US$2–3 per Chinese citizen per year. By contrast, OECD estimates put average pandemic prevention, preparedness, and response spending at around US$101 per capita, with the United States at US$279 and Germany at US$209. The true gap must be smaller, since China adds money through provincial budgets, immunization programs, and other health lines that don’t show up in the MOF subsidies, but I estimate that the sum of these monetary investments still falls well below the OECD average.

How China Talks About the US

One interesting factor shaping China’s pandemic governance has been its rhetorical positioning vis-à-vis the United States.

Beijing has leaned heavily on the narrative that America’s COVID response was chaotic, politicized, and unscientific, using US failings as a foil to validate its own system. The strategy deflects criticism of China’s early missteps and reinforces the idea that China’s centralized model is not only legitimate but superior.

For example:

A People’s Daily editorial from May 2025 calls the US the “全球第一抗疫失败国” (literally: “world’s No. 1 failure in pandemic response”), citing CDC death totals and arguing that the outcome exposes pseudo-science.

A post on the National Health Commission’s website accused the US of “squandering time” and policy ineffectiveness.

A Global Times editorial said, “As the world’s most developed country, its response to the pandemic has been a complete failure, offering no positive lessons.”

This narrative has political uses, but it could also make Beijing overconfident. By defining itself in opposition to the US, China has built a pandemic story that depends on its own perceived success, which could also make addressing institutional shortcomings difficult.

For instance, Chinese state media outlets have often disparaged the effectiveness of US vaccines, framing Western rollout efforts as reckless or unsafe. Yet beneath those critiques lies the unspoken acknowledgment that during COVID-19, China’s vaccine sector fell far behind its Western counterparts in both technology and trust. Beijing’s decision to reject mRNA vaccines like Moderna, despite their demonstrated efficacy, left millions reliant on weaker domestic shots.

Meta-Grade: China is grading its own paper here, and giving itself full marks despite doing a lousy job of handling COVID. Revising history, rather than addressing one’s mistakes, tends to be a bad idea.

International Moves

China has also engaged in a series of international initiatives on pandemic preparedness, though international communiqués on public health are rarely binding. Xi’s Global Security Initiative, for example, claims China will lead international biosecurity, but says little about how it will actually accomplish this.

Funding is a clearer signal. In May 2025, China pledged $500 million to the WHO over five years, effectively becoming the organization’s largest funder after the US withdrawal. China has also contributed to many other initiatives, like the World Bank’s Pandemic Fund, and hasn’t abstained from other multilateral health financing mechanisms (unlike the US).

A substantial portion of China’s health funding targets the Global South, particularly in Africa. China committed $80 million for constructing an Africa CDC headquarters in Ethiopia, a project that became operational during the pandemic, and $2 billion in assistance for COVID-19 response and economic recovery in developing countries. China’s WHO funding notably includes the condition of “a certain amount of voluntary contribution and projects support through the Global Development and South-South Cooperation Fund” — terminology tied to China’s Health Silk Road initiative, essentially the public health dimension of the BRI. 52 out of 54 African countries have participated in these health programs.

China has also recently convened ASEAN Conferences on biosecurity governance in conjunction with the UN Office of Disarmament Affairs. These talks emphasize lab safety, pathogen-sharing, and early-warning systems between South East Asian countries.

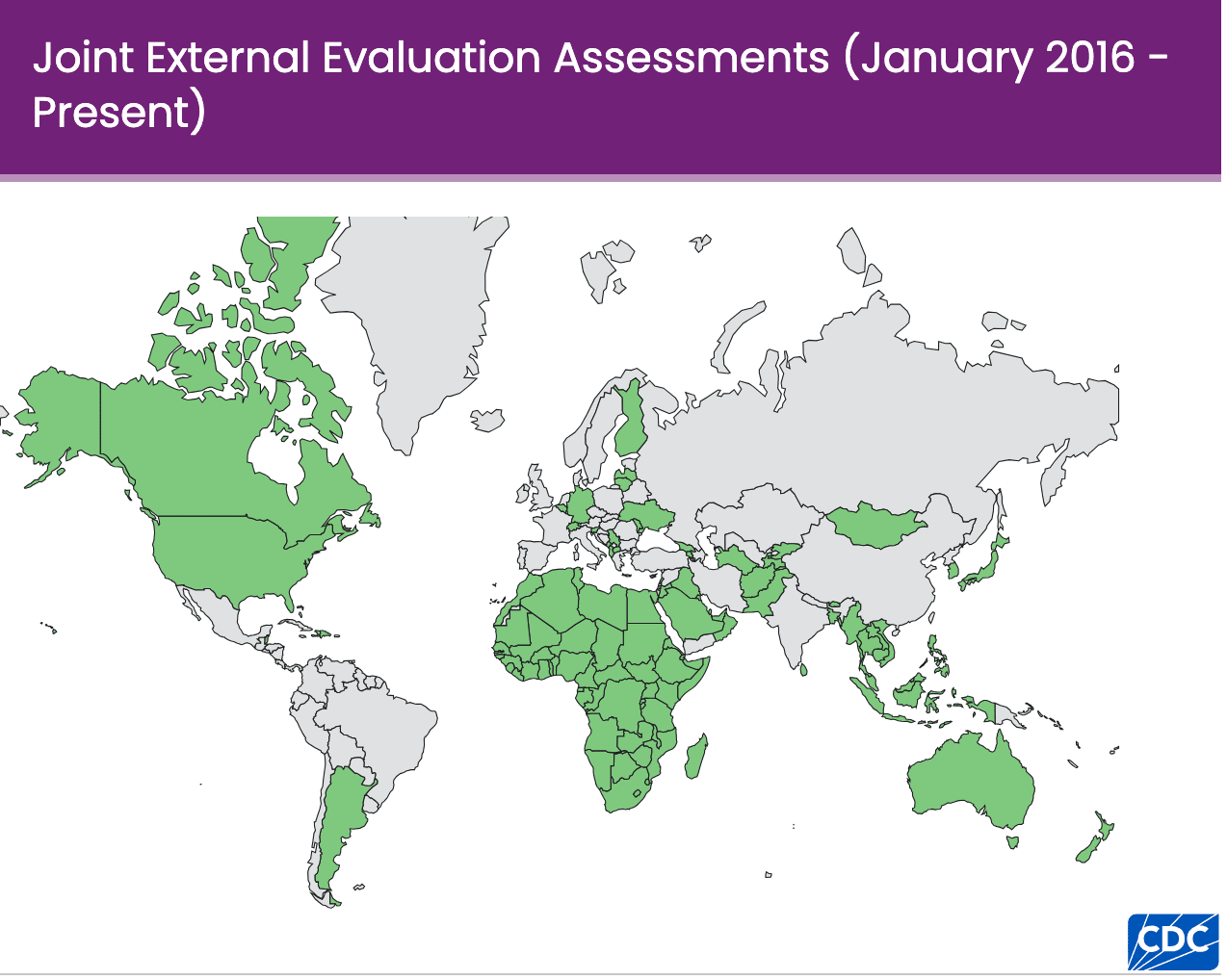

Despite positioning itself as a global health leader, China consistently fails to report the specifics of its assistance activities to international agencies like the OECD’s Common Reporting System or the International Aid Transparency Initiative. Tensions have also flared with organizations like the WHO over China’s lack of timeliness, completeness, and durability of data sharing, especially around origins-relevant evidence for COVID and during recent disease surges. In November 2023, for instance, the WHO formally requested detailed information on pneumonia clusters among children following reports of cases in northern China. Beijing eventually provided data, but only after a significant delay, underscoring a pattern of reactive rather than proactive disclosure. China furthermore does not participate in Joint External Evaluation Assessments, where a team of independent international experts evaluates a country’s health security capabilities across 19 technical areas.

I believe this kind of behavior makes sense when accounting for how central reputation and “saving face” are to China’s public-health motivations. Reporting outbreaks quickly or exposing gaps in its own system can be embarrassing; projecting itself as a global public health advocate and generous benefactor to the Global South is not. If China can manage its own health problems internally and fund other systems externally, it (1) looks good and (2) reduces outside scrutiny — a bit like a boyfriend who pays for dinner so his girlfriend doesn’t go through his phone.

Grade: C

They say all the right things, and it’s good they’re helping the Global South’s public health infrastructure, but they still avoid building the deeper collaborative foundations we’d need for a globally unified response to a major infectious outbreak.

Conclusion

The CCP is taking pandemic readiness seriously, but the through line isn’t a coherent strategy so much as a collection of post-COVID impulses: prevent another global pandemic from originating in China, avoid another round of draconian lockdowns, and do it all without loosening Beijing’s grip while empowering people to speak up.

Call to action

If you know anything about this topic or think I’ve missed something important, please reach out. I’m particularly interested in hearing from people with knowledge about China’s vaccine development capacity, high-end PPE manufacturing, biosurveillance systems, or research and safety standards for future installments.

I did not find nearly as many experts on Biosecurity x China as I would have liked. China’s pandemic preparedness apparatus remains surprisingly under-studied, especially compared to the extensive analysis of its COVID response or the pandemic readiness systems of other countries. The expert on this could be YOU.

Follow up to: nick@chinatalk.media

ChinaTalk is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

The broader Emergency Response Law (突发事件应对法) still seems to be responsible for certain types of pandemic emergency situations, but the two new laws appear to have taken over many of the responsibilities this law originally covered.

Chloe Lee wrote a strong analysis of the Biosecurity Law and Regulations on the Export Control of Dual-Use Items as they existed before the 2024 updates, laying out some of their weak points.

{kind=link}